Abstract

The Council of Financial Regulators has released an “Issues Paper” in response to the federal treasury’s instruction into the competitiveness of the Australian Banking industry and the part that smaller banks have to play. The paper calls for recommendations to be submitted by February 7th 2025.

The issues paper highlights the concentrated nature of the Australian banking market where 4 banks own 80% of the deposit market and 90% of the mortgage market, along with strategies for small to medium-sized banks to focus on in order to scale and compete: Increase Use of Digital Channels, Merge and Collaborate, Outsourcing and Joint Ventures.

To level the playing field and enhance competition, five government strategies are recommended by Moroku around:

- Capital Treatment

- R&D Provisions

- Financial Inclusion

- Digital Identity and

- Open Banking

By the government implementing these measures, we believe that smaller banks can better serve their communities, drive financial industry competitiveness, and support economic growth.

Background

On the 8th of July, The Australian Federal Treasurer, Jim Chalmers, issued a letter of instruction to the Governor of the Reserve Bank, as Chair of the Council of Financial Regulators (CFR), to conduct a review of the small and medium-sized banking sectors. In the letter, the Treasurer noted that small to medium sized banks play an important role in our communities, supporting households and businesses as well as the competitiveness of the industry. With a range of current and emerging challenges facing small and medium-sized banks the Treasurer sought views from the CFR on how the Government could better support competition and dynamism in the banking industry, including what steps might be taken to bring increased proportionality and an appropriate balance between competition, innovation and stability.

An “issues paper” has now been released by the Council seeking submissions by the 7th February 2025. The letter of instruction comes against the backdrop of the ever booming residential property market and with it borrowing. Capital growth on Australian residential property in the last 12 months amounted to $800bn, significantly bigger than the entire Federal Government budget and 5X the earnings of every company on the ASX combined. Australia’s economy is built on holes and homes. The lucky country continues to have the minerals the world’s industrial machines yearn for, combined with a lifestyle that is the envy of many. Despite the high cost of home ownership, Australia’s employment rate of 64% is significantly higher than the G20 average of 54%, though its poverty rate of 13.4% is also higher than many other G20 countries with 3.3 million people, including 761,000 children, living below the poverty line.

Off the back of this growth, the Australian banking industry has seen significant profit over the last 12 months. The big four banks—Commonwealth Bank of Australia (CBA), Australia and New Zealand Banking Group (ANZ), Westpac Banking Corporation (WBC), and National Australia Bank (NAB) have reported a collective profit of over $40bn, bolstered by increased net interest margins (NIM) due to higher interest rates and climbing house prices, improving interest income on loan portfolios.

The issues paper highlights a number of points:

- Lending is the main source of revenue for banks and whilst making large profits, the large banks have given up some share

- Lending is primarily funded by the financial markets, but in the small banks it is driven almost exclusively by deposits, largely because they don’t have access to the financial markets

- Brokers source a large proportion of loans but the smaller banks aren’t in this distribution chain.

- Technology is a primary driver of competition, enabling customers to switch apps quickly for greater capabilities, and again is an area where the larger banks have a significant advantage.

To drive more financial inclusion and industry competition smaller banks need to increase their deposits, have greater access to alternative funding sources and technology systems that allow them to compete, provide compelling digital experiences to customers and connect to the broader ecosystem such as brokers. Governments have sufficient power to unleash smaller banks to do their work here. Do they have the will?

Lending

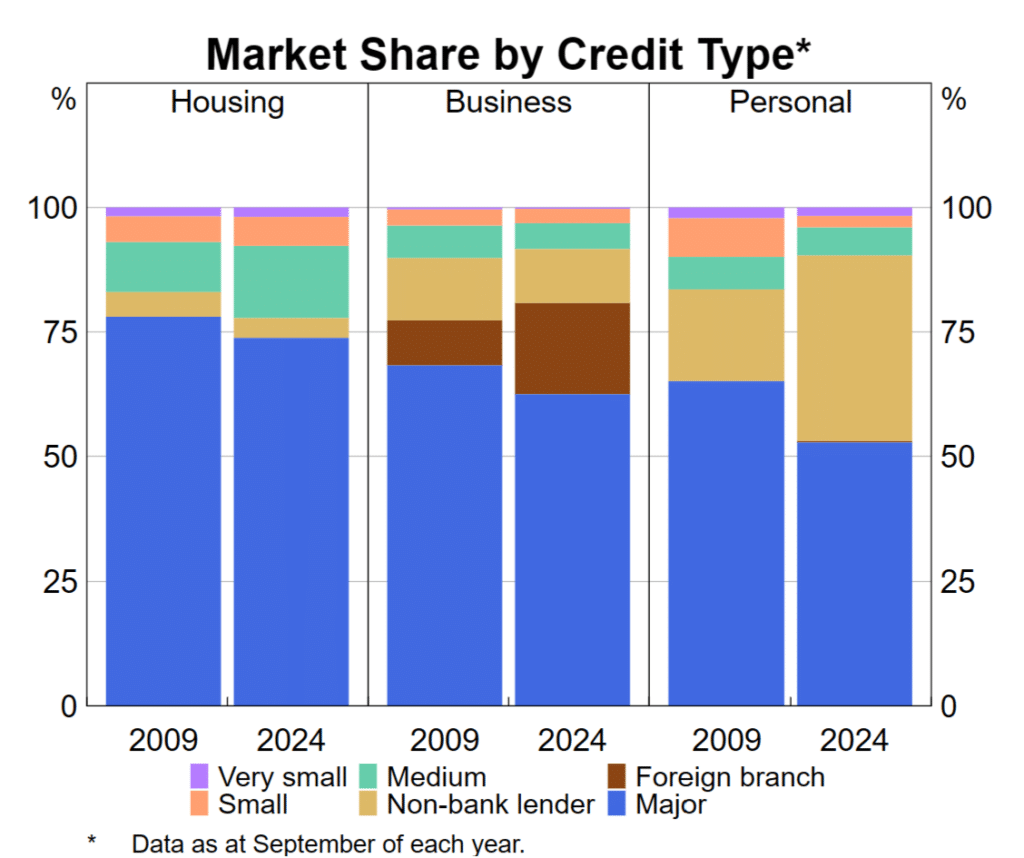

Lending is the main source of income for Australian banks. It currently represents 85% of revenue, up from 70% in 2011. The major banks have given up some mortgage market share to the small and medium sized banks as the impacts of interest rate hikes and Open Banking kick in, making customers more price sensitive and the big banks strangle hold on decisioning data is removed.

Non-bank lenders have been the biggest winners, increasing their share, mostly in lending to small and medium enterprises (SMEs). Personal lending constitutes only 5% of total credit, with non-bank lenders comprising around a third of this.

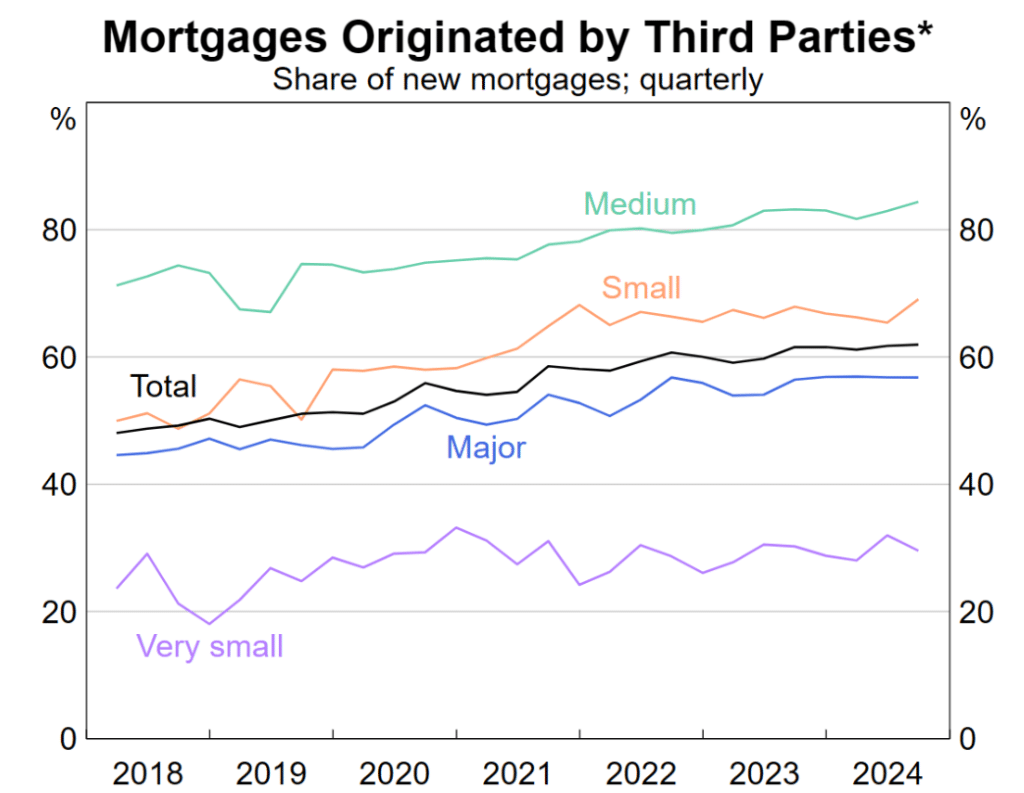

In home lending, brokers have become an increasingly important source of origination, as well as lowering the barriers to customer switching. In the first half of 2024, around 60% of mortgages were written via brokers.

Small and medium banks source a greater share of new mortgages from brokers than the major banks, but very small banks only originate a quarter of their new mortgages via brokers.

Funding

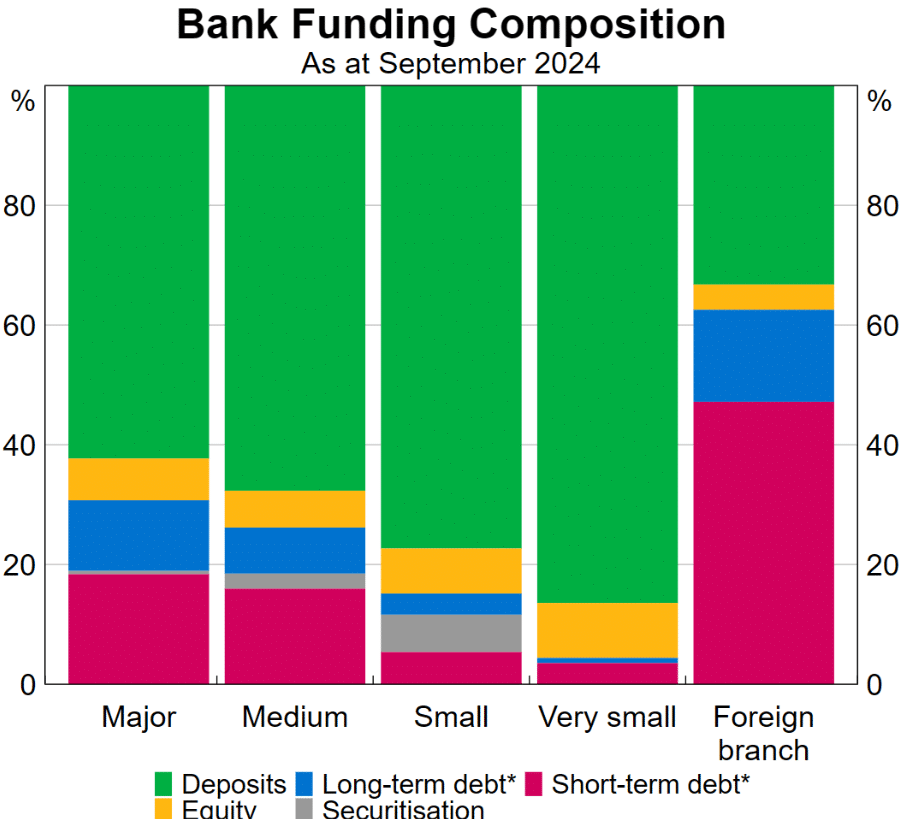

Smaller banks have a high dependency on deposits and in order to gather them they need great digital experiences that encourage deposits, Main Financial Institution status and saving.

On average, domestically incorporated banks source more than half their funding from deposits, and this share has increased steadily over the past decade. Australian consumers depend on retail deposit products to conduct their everyday banking, to safely store over $1.4 trillion of their savings and earn a decent return on these funds.

Use of deposit funding tends to be negatively correlated to the size of the bank; the smallest domestic banks typically have the greatest share of their funding in deposits, while larger banks access a broader range of domestic and international funding sources. Smaller banks’ growth plans are therefore strongly linked to their ability to attract additional deposits.

Mutual banks rely primarily on retained earnings to increase capital, as they cannot issue ordinary shares consistent with their mutual structures. This constrains their ability to expand their balance sheet quickly.

Since 2018, mutual banks have also been able to issue mutual equity interests or Mutual Capital Instruments, that meet the requirements for Common Equity Tier 1 (CET1) capital, but there has been very little issuance to date for several reasons:

- Regulatory Limitations: APRA has imposed certain limitations, including a cap on the level of MEIs that can be included in CET1 capital. This restricts the amount of MEIs mutual banks can issue.

- Market Conditions: The market conditions and investor sentiment have not always been favourable for issuing new equity instruments.

- Cost of Issuance: Issuing new equity can be costly and may dilute the value of existing members’ interests.

- Regulatory Uncertainty: APRA’s intention to phase out bank AT1 capital instruments and a disclosed intention to improve proportionality with a simpler approach and lower capital requirements for smaller domestic banks keeps boards capital strategies on hold.

- Alternative Capital Instruments: Mutual banks may prefer to use other types of capital instruments that are less costly and meet regulatory requirements

Technology

Technology innovation is a key driver of competition and smaller banks need help to fund this innovation

Technology is emerging as a key driver of competition in banking. Customers, particularly those who are younger, are increasingly switching to banks due to the technology offering, with a strong focus on streamlined apps and websites.Technology can also support efficiencies, allowing banks to on board customers more easily, process loan decisions more quickly and engage with customers across channels.

Banks are spending a larger share of operating expenses on technology to automate processes and to meet customers’ preference for digital channels. Technology expenses include adopting new technologies such as API-enabled architectures and cloud-based services, as well as responding to growing challenges such as scams and cyber threats.

Smaller banks can face significant challenges, given smaller technology budgets and heightened costs and risks associated with replacing legacy systems.

For small and medium banks to compete with large banks, technology investment is required to:

- apply innovation in the sector;

- meet consumer demands for accessing banks via digital channels;

- maintain existing systems;

- meet new regulatory requirements; and

- address emerging scam and cybersecurity threats.

Switching

Switching banks is difficult and the government can do more to remove the friction

Despite the Productivity Commission in 2017 pointing out that customer friction in switching is a major restraint to industry competitiveness, the ACCC in December 2023, confirmed that consumers still find it difficult to switch accounts, so most do not. Relatively few consumers switch deposit products, despite there often being a range of alternative products offering better interest rates and conditions. There are significant impediments to switching which take time and effort to overcome, and which occur at several points in the process. These include changing direct debits and other recurring payments, redirecting incoming payments and proving identity.

There have been a number of initiatives to date that have so far been ineffective at addressing both barriers to switching, and barriers in consumer engagement more generally:

- Account Switching Package (2008): Introduced by the Rudd Government, this package included measures like a listing and switching service, a single consumer complaints hotline, consumer education resources, and an industry review of entry and exit fees.

- Consumer Data Right (CDR): Launched in 2019, the CDR allows customers to access their data and share it with other financial institutions, making it easier to compare and switch banks.

- Government ‘Nudge’ Initiatives (2024): The federal government has required banks to provide clearer information about deposit rates and simplified the process for switching home loans.

Banks must also notify customers when their savings interest rates change.

Measures that could reduce or remove these barriers have the potential to facilitate more widespread competition between banks and enhance consumer outcomes in the retail deposits market. Switching electricity providers in Australia has become relatively straightforward due to market deregulation and new rules introduced by the Australian Competition and Consumer Commission (ACCC). The methods offer key insights for how to reduce switching friction in banking:

- Ease of Switching: Customers can switch electricity providers within 48 hours. This is a significant improvement from the previous process, which could take up to 90 days.

- Comparison Tools: Various comparison websites and services help customers find better deals and switch providers easily. This includes price but more importantly “value”

- No Disruption: The switch is usually seamless, with the new provider handling most of the administrative work.

In contrast, switching banks in Australia, while also facilitated by government initiatives like the Consumer Data Right (CDR), can still involve more steps:

- Direct Debits and Payments: Customers need to manually transfer direct debits and set up new payments.

- Multiple Accounts: Often, customers have multiple accounts (savings, checking, loans) that need to be switched over individually.

- Customer Service: The process can be more complex and may require more direct communication with both the old and new banks.

Overall, while both sectors have seen improvements in switching processes, switching electricity providers is generally quicker and less cumbersome than switching banks and more work is required by the regulators to drive switching parity between the utility and finance sectors.

Opportunities for scale

The issues paper highlights 4 strategies for small to medium sized banks to focus on to achieve scale and compete:

- Increase use of digital channels

- Merge

- Outsource

- Joint Ventures

Increase use of digital channels and investment in technology

Digital channels and new technology may present opportunities for small and medium banks to compete against the major banks, particularly in niche market sectors. Digital channels can make it easier for banks to connect with customers and onboard them quickly, enabling access to a potentially broader customer base. Investments in technology can be made to process loan applications quickly and make the bank more useful for customers and brokers.

However, the paper notes that small and medium banks with legacy systems may encounter challenges in keeping pace with technological offerings of new entrants or the larger banks.

Merging and collaboration to achieve the benefits of scale

The pursuit of economies of scale and other efficiencies may lead small and medium banks towards consolidation. A number of mergers and acquisitions have occurred amongst banks in the past two decades but these have routinely been amongst the larger of the small banks with the smaller ones running the gauntlet of independence. Banks consolidate to achieve scale at speed, and at a lower cost than investing in organic growth.

Entities that have advanced digital investments and capabilities, to achieve portfolio diversification, integrations, efficiencies, scale will present merger and collaboration opportunities to grow and compete.

Outsourcing to achieve the benefits of scale

Outsourcing has become a key focus for all banks. By engaging third-party service providers, small and medium banks can access advanced technologies and specialised expertise that would otherwise be prohibitively expensive, or complex to develop and maintain internally. This includes critical skills in essential areas that enable banks to offer compelling digital banking services including system integration and marketplace integration, cyber response and network design.

Joint ventures or strategic alliances

Joint ventures or strategic alliances with other banks can be a useful way for smaller banks to reap the benefits of scale, without undertaking a merger or acquisition. These approaches can enable banks to pool resources, tap into broader expertise, and leverage their combined market bargaining power. Examples could include shared operating platforms. With the shift to more digital banking, there could be a stronger impetus to explore these options. The Review is seeking feedback from industry on whether there are potential impediments to using these options.

Recommendations

With technology being so critical to competition and dynamism and the bigger banks capital advantage being a big part of the answer Moroku recommends the government adopt a number of strategies to level the playing field:

- Capital Amortisation & Options

- R&D

- Financial Inclusion

- Digital identity and MyGov

- Open Banking

Capital Amortisation & Options

Mutual organisations often face stringent regulatory requirements that limit their ability to amortise capital expenditures and free up capital for lending. These regulations can make it difficult for mutuals to invest in new projects and infrastructure and grow their loan books.

- Tax Treatment: The tax treatment of capital expenditures can be unfavorable for smaller banks, making it less attractive to amortise these costs.

Limited Capital Raising Options: Historically, mutuals have been restricted in their ability to raise capital, often relying on retained earnings or debt. This limits their capacity to invest in new projects and amortize capital expenditures.

Member Approval Requirements: Mutual organizations typically require member approval for significant financial decisions, including capital expenditures. This can slow down the process and make it more challenging to amortize capital.

Potential Solutions

- Simplifying Regulatory Requirements: Streamlining regulatory processes can help mutuals manage capital expenditures more efficiently.

- Amending Tax Treatment: Changes to the tax treatment of capital expenditures could make it more attractive for mutuals to amortize these costs.

- Expanding Capital Instruments: Allowing mutuals to issue a broader range of capital instruments, such as Common Equity Tier 1 (CET1) capital instruments, could provide more flexibility in raising funds.

R&D Provisions

The Research and Development (R&D) Tax Incentive in Australia is a government initiative designed to encourage companies to engage in R&D activities by offsetting some of the costs associated with eligible R&D. The main purpose of the R&D Tax Incentive is to boost competitiveness and productivity across the Australian economy by supporting innovation and technological advancement. Currently, if the R&D expenditure is less than $20,000, smaller banks can work with a Research Service Provider to conduct the R&D activities. The scheme should be reevaluated to increase this limit and other measures to encourage smaller banks to invest in segment specific innovations, including collaborations to drive innovation and boost competitiveness.

Financial Inclusion

The essential nature of life is all inclusive.

To promote financial and social inclusion, poverty reduction, and home ownership among lower-income groups, smaller banks, which serve their communities deeply, should be better empowered, by the government, to take on this challenge. Capitalist governments, like in Australia, largely exist to provide services that the market doesn’t. Banking the udnerservered and under banked is a classic opportunity for government presence. Potential support, bythe government for smaller banks to support financial inclusion covers a range of grants enabled by technology to speed access.

This could involve an API-enabled TFN/MyGov register for first home buyers and low-income earners to register through a small bank loan application. When they apply for a loan, their identity and home ownership status would be verified, with government grants and subsidies automatically applied during the loan application process. Upon approval, the status would be updated, and the scheme’s performance measured.

Limiting this to small banks would enable them to deploy capital competitively into this crucial segment, where they have a mandate, unlike bigger banks.

By promoting digital access to financial services, linking them to home ownership grants, implementing real-time digital government guarantees, and offering tax incentives for smaller banks to serve the financially excluded, innovation can be unleashed.

Engaging fintechs to build these systems, rather than traditional government outsourcers, would drive financial industry competitiveness and innovation, ultimately benefiting Australia’s low-income segments.

Digital Identity

Customer onboarding remains a key aspect to customer switching. MyGovID and other digital identity services such as NSW Services App needs more investment to make it an accessible and available part of KYC so that the baroque drivers license and passport identity check friction can be removed.

Open Banking

Improving Australia’s Open Banking Consumer Data Right (CDR) regime to drive competitiveness and facilitate account switching can be achieved through several key measures:

- Enhanced Data Sharing: Expanding the types of data that can be shared under the CDR regime to enable them to switch accounts. This means including Bill Payment, Direct Debit Information so that it can all be transferred to a new bank for the switch

- Simplified Consent Process: Streamlining the consent process for data sharing, using App to App and other mechanisms to reduce friction for consumers.

- Bi-Directional – Enabling payments within Open Banking so that the smaller banks app can not only read data from other banks but instruct payments

By implementing these measures, Australia’s Open Banking CDR regime can become more competitive and facilitate easier account switching, ultimately benefiting consumers and promoting financial innovation.

About Moroku

Moroku is an Australian SaaS engagement and loyalty platform that uses game and data to enable financial services providers to differentiate and create value by taking their customers on a journey of money mastery. Moroku’s vision is of a world where everyone is being great with their money. To do that, financial services need to be fun and social. When service is this way, people pay attention, get curious, overcome challenges, grow skills, and go on a journey of mastery. Moroku’s platform and processes create engaging financial services experiences for banks and wealth providers that empower customers and help everyone win. Moroku executes with a growing set of IP based around:

- On-Ramp, its proprietary design sprint methodology, is conducted as a service engagement with financial service providers to define a game based digital user experience. The outcomes are a tested prototype and proposal for productionisation.

- Odyssey, cloud based, application engagement platform that drives the user experience, getting users to pay attention, build financial muscle and act.

- Money, its white label digital banking platform that includes core banking, mobile and internet banking, loan origination and management