The era of mass production is over. Power is shifting to the consumer, who want less choice and more understanding of what they want, where they want it, how and when. Nike is leading the way from providing customers with choices to giving them control over product, the move from mass production to mass customisation and the segment of one. Whilst retailers have been shifting product design to the customer, financial services have been slower on the uptake. With data systems now in place, personalisation engines are increasingly using the available customer insight to tailor services for individual customers at scale in digital.

A recent Capco research report states that 72% of customers expect to receive personalised banking experience, including financial advice based on their income level, spending habits, and saving goals. The ability to personalise banking experiences is a key expectation among bank customers today, according to the report.

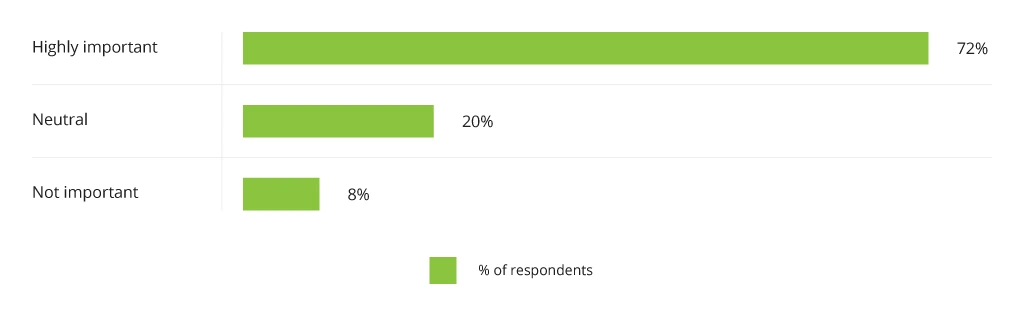

Importance of a Personalized Banking Experience for US Customers

Personalization – here comes the next generation of banking CRM: It’s a win:win

The desire for customers to personalise their banking relationship is the strongest message emerging from the survey.

- 72% of respondents rated personalisation as “highly important,” while just 8% said it was not.

- 20% of respondents were neutral on the topic.

- Millennials place the highest value on personalisation (79%), followed by 75% of Gen Z, 74% of Gen X, and 58% of boomers.

- 86% of people who felt personalisation is important to their experience are willing to provide feedback on their experiences at least annually.

- Customers who are older and have higher income levels are more willing to provide regular feedback.

According to Deloitte, hyper-personalisation can be defined as using real-time data to generate insights by using behavioural and data sciences to deliver services, products and pricing that are context-specific and relevant to customers’ manifest and latent needs (i.e., those needs which, due to a lack of information or availability of a product or service, cannot be satisfied).

While personalisation is already used to analyse data arrays after a specific action of the user (for example, visiting a loan’s section on a banking website), hyper-personalization is powered by a more extensive set of data that is customer success focussed.

Equipped with customer information, data models establish and then increasingly personalise digital customer profiles that can be used to offer individualized services that cater to the users’ changing needs.

Hyper-personalised services are proactive, embedding hypotheses on where customers are going, based on where they’ve come from, where they are, behavioural analysis around the direction they are heading and any course correction or support they may need or be looking for to get there. Such a proactive approach, anticipates the customers’ needs to deliver the support, encouragement and reward to stick at it. In this paradigm it is less about the delivering the right product at the right time and more about the right help at the right time using the veridical propensity model. For instance, if a customer browses car loans via their mobile app, the old model would look to come up with a tailored loan. In the new model, we prepare and reward the customer to save up for the deposit for that loan and do so in a manner that is more success focussed.

Tactical versus strategic personalisation

Payment transactions are a treasure trove of information. Increasingly rich transaction data such as merchant category code (MCC), merchant name and basket related data such as product can then be augmented with categorisation engines to show what customers bought when, where, what they paid for it , what category of product it was and how often they are making that purchase. Such insights can then be used to identify savings and loyalty opportunities. These are tactical personalisation opportunities, sniffing out tactical engagements based on a narrow rule set. We see these types of solutions cropping up to help people save money on category purchases (financial products, retail products such as saving money on petrol, transport, food, entertainment etc) and which are most easily identified by those looking to craft offers such as “I see that you have been regularly buying XXX, you can save $2.5 per week by buying your XXX here”; – classic tactical personalisation.