The Role of Regression Models in Loan Origination: The Foundation for the future of lending

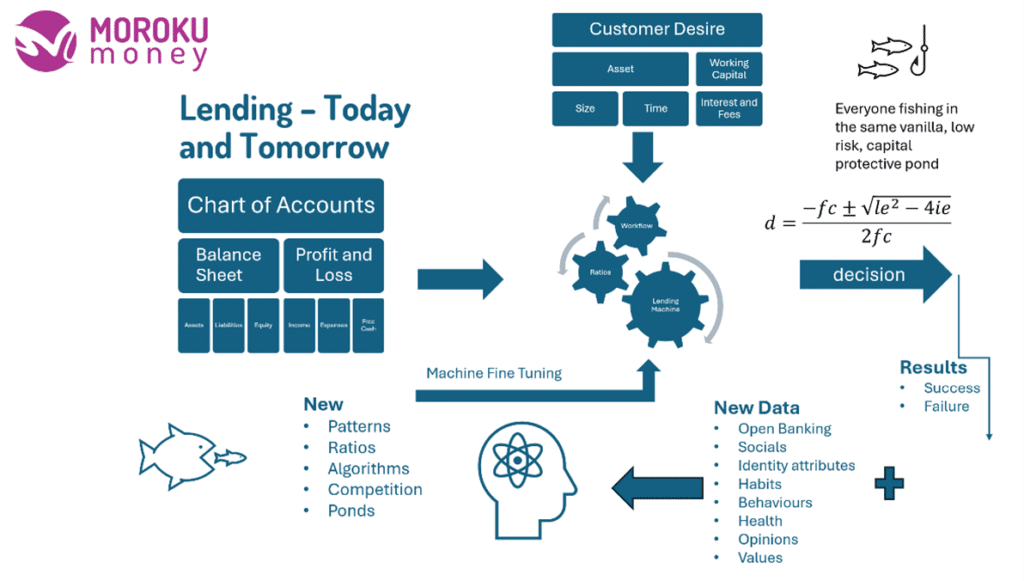

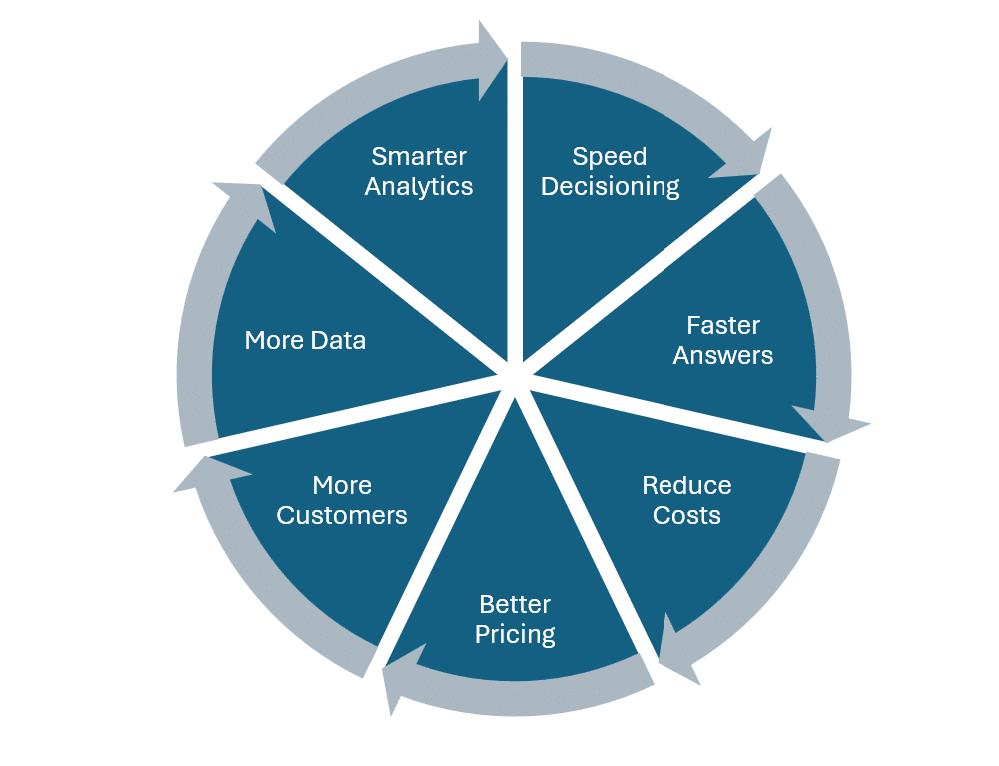

Competitiveness in lending is predicated on decisioning speed – Saying Yes or No as fast as possible. Those that can use advanced analytics to speed decisioning will capture share by providing answers faster to eager customers, reduce costs by reducing headcount, enabling them to provide better pricing and capture more share. More customers creates more data that drives better decisioning in in a wheel of prosperity. Whilst large organisations get this and are building large data science teams, imagine if such a capability was available on a subscription basis, as a service.

Whilst there is a lot of work going on to automate workflows, the ROI of these investments is dependent on the accuracy of the underlying risk engines. This accuracy requires the risk team having a robust and granular understanding on the relationship between the inputs and the outputs of the risk model. This is to say that there is a high degree of knowledge and understanding between who the customer is, their position and the loan they are after and whether to lend to them. The finer grained this is, the greater the understanding of the correlation betwene the inputs and the outputs, the less data is required as only the actual data that actually matters is requested and processed, making the application and decisioning processes faster.

A key tool in building this intelligence is the regression model. These models, provide the statistical correlation for the system and lay the groundwork for the integration of more advanced artificial intelligence (AI) technologies in the financial sector.

Unfortunately much of this work has not been updated within lenders for some time, leading to a cognitive disodance, the collection of more data than may be necessary and slower decisioning. Without updated correlations, automation hits a a massive speed bump.

Understanding Regression Models

A regression model is a statistical technique used to predict the value of a dependent variable based on one or more independent variables. In the context of loan origination, the dependent variable could be the likelihood of default or the loan amount or the decision to lend the customer money or not. The independent variables include the applicant’s income, credit score, employment history, and financial position.

There are several types of regression models, but the most commonly used in loan origination include:

- Linear Regression: This model predicts the value of the dependent variable as a straight-line relationship with the independent variables.

- Logistic Regression: Often used when the dependent variable is binary (e.g., whether a loan will default or not), this model estimates the probability of a particular outcome.

- Ridge and Lasso Regression: These models are variations of linear regression that include regularisation terms to prevent overfitting and improve the model’s accuracy.

How Regression Models Work

Regression models work by identifying relationships between variables. In loan origination, the process typically involves the following steps:

1. Data Collection: Gather a comprehensive dataset containing historical loan data, including borrower information and loan outcomes.

2. Feature Selection Identify the most relevant features (independent variables) that influence the dependent variable (e.g., loan default).

3. Model Training: Use the historical data to train the regression model. This involves finding the best-fit coefficients for the independent variables that minimize the prediction error.

4. Model Evaluation: Test the model using a separate dataset to evaluate its accuracy and effectiveness in predicting loan outcomes.

5. Prediction and Decision-Making: Apply the trained model to new loan applications to predict outcomes and make informed lending decisions.

Why Regression Models are Important

Regression models are crucial in loan origination for several reasons:

- Risk Assessment: Referession models help financial institutions assess the risk of lending to a particular applicant by predicting the likelihood of a customer to repay the loan and therefore whether to lend them money.

- Decision Consistency: By relying on mathematical models, lenders can ensure consistency and objectivity in their decision-making processes, reducing the potential for human bias.

- Regulatory Compliance: Financial regulators require lenders to use transparent and explainable models in their credit decisioning processes. Regression models are easy to interpret and justify to regulators using statsistical data to explain whythey use the models and the results they are getting as oppsoed to saying, “Its what we’ve always done, it seems to work”.

- Efficiency: Automating the risk assessment process with regression models streamlines loan origination, enabling quicker and more efficient decision-making.

- Cost Savings: By accurately predicting the risk of default, lenders can minimise losses and allocate capital more effectively, ultimately improving profitability.

- Competitiveness: By using regression models, lenders build mastery in the connectionbetweentheir unique market segment and their lending policies, allowing them to personalise credit for them and their market and out compete the corse grained mass market players

Foundations for AI in Lending Decisioning

While regression models are powerful tools on their own, they also provide the foundation for more advanced AI technologies in lending decision-making. Here’s how:

1. Data-Driven Insights: Regression models help financial institutions develop a data-driven approach to decision-making, which is essential for integrating AI technologies.

2. Feature Engineering: The process of selecting and engineering features for regression models builds expertise in handling and processing data, a skill that is critical for developing AI models.

3. Model Interpretability: Understanding how regression models work and their limitations aids in developing AI models that are transparent and interpretable, addressing regulatory and ethical concerns.

4. Incremental Improvement: Financial institutions can start with regression models and gradually integrate more complex AI models (e.g., neural networks, decision trees) as they become more comfortable with data-driven decision-making.

5. Hybrid Models: Some advanced AI models combine regression techniques with other methods to create hybrid models that leverage the strengths of multiple approaches for improved prediction accuracy.

Regression models have long been a cornerstone of risk assessment in loan origination. They provide a robust, interpretable, and efficient means of predicting loan outcomes and making informed lending decisions. As financial institutions increasingly adopt AI technologies, regression models serve as an essential foundation, bridging the gap between traditional statistical methods and cutting-edge AI solutions. By leveraging these models, lenders can enhance their decision-making processes, reduce risk, and stay competitive in an ever-evolving financial landscape.