Younger consumers perception of credit unions has worsened as member owned banks fall behind the big banks in account openings and relevance. Socially centric digital offers hope.

This is according to a recent McKinsey report that calls out customer service, better interest rates, and support for their community as Millennial’s top reasons for changing and choosing a financial institution. This presents a real opportunity for the mutual sector to drive relevant digital experiences that demonstrate social impact as a strategic initiative. All the big hot button issues for millennials (i.e. people in their prime borrowing years) are within reach of better digital.

The report highlights 5 trends and 6 opportunities that the member owned banking segment should take notice of. To grow, credit unions must appeal to younger segments by doubling down on consumer engagement, digital enablement, modernisation of legacy platforms, and acquire new scale and capabilities through M&A and partnerships.

5 Trends

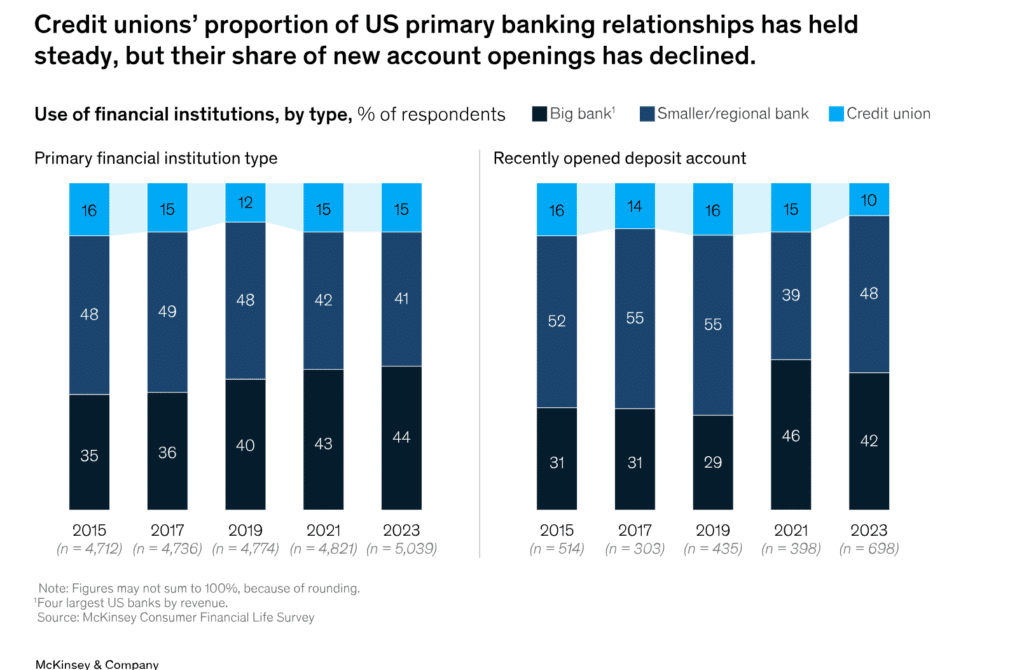

Credit Union share of account openings is falling: Credit Unions are losing share to big banks primarily due to differences in digital capabilities to reach and rapidly convert consumers online.

Credit Unions are losing ground with younger generations, as they become top heavy in a dying category of customers, Baby Boomers, whilst losing Gen X and Millennial share to the bigger banks.

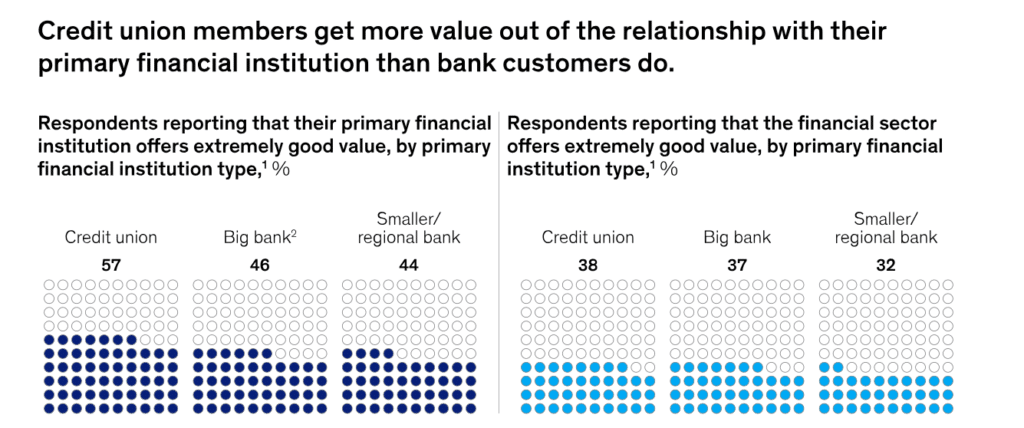

Members of credit unions see a lot of value in them. Despite the decline, existing members see more value in the credit unions than bank customers do.

Younger consumers are not big fans of credit unions. They are finding less value in credit unions as they get older, acquire more assets and their expectations concerning digital capabilities shift. They will switch for a superior mobile banking app and a superior online banking website. These are areas where the bigger banks excel and credit unions must improve.

Credit Unions have a significant opportunity to attract younger members. Better customer service, better interest rates, and support for their community are driving younger customers to move bank. This presents a major opportunity for credit unions to connect with these customers around a message of commitment to service, favourable rates, and a sense of community.

6 Opportunities

Social Impact: Younger customers are more value-conscious than older generations, subject to switching to support their communities, more likely to purchase goods or services from businesses that prioritize social and environmental responsibility and commitment to strengthening communities, protecting consumers, and ensuring financial inclusion.

Digital Channels. Beyond standard banking functions, younger consumers do their research and are influenced online. Financial inclusion is a big issue and opportunity to embed content and services that help customers understand their money and support strong habits, building credibility as stewards of financial well-being.

Personalisation: Develop distinctive, targeted loyalty and rewards programs, that back up the story around community, social impact and financial inclusion.

Core Technology: Create a platform strategy that is tied to specific business cases, such as revenue generation or user experience, whilst simplifying and rationalising products and features prior to migration, coupled with a focus on improving user experiences

AI. Reimagining all parts of the business to meet younger consumers’ needs. McKinsey estimates that AI could deliver as much as $1 trillion in additional value for the global banking market annually, and roughly three-quarters of that total stems from the “four Cs”: customer engagement; coding; concision (synthesizing insights from data) ; and content generation.

M&A and Partnerships. There are 4,600 credit unions in the USA, including nearly 4,000 with assets of less than $500 million. In Australia, 30% of the market has less than $500M. M&A with other mutuals must be a focus to drive efficiencies as well as with fintechs to acquire new capabilities and relevance.