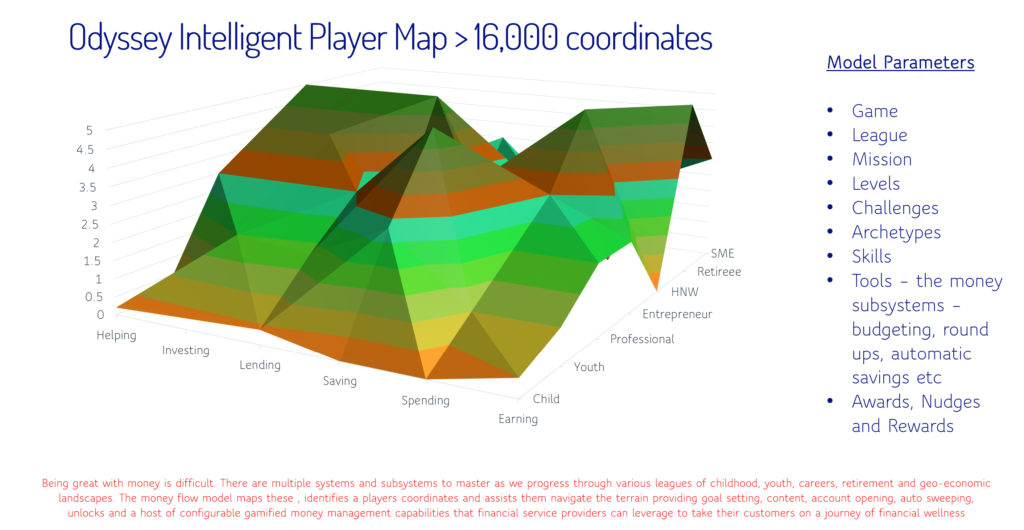

Using game as a journey architecture helps customers take on their money missions, whilst rewarding strong money habits and deepening customer relationships.

Moroku help banks win by helping their customers win. We do this by building digital experiences that motivate customers to build strong money habits and through this model build sustainable banking businesses based on liquidity as opposed to net interest income (NII) and fees. This is both really important and really hard.

This is really important because as we enter a period potentially more grave than the Financial Crisis of 2007/2008 , more people will fall under financial stress unless they focus on the fundamentals. Win/Win serves as a very good lens by which to build customer relationships and value beyond NII. Win/Win demands that we are focussed on helping customers with a problem and build a business by solving that problem well.

The average savings at retirement in Australia is $130,000, hardly enough to last 20 or 30 years in a country where every man, woman and child owes on average $2000 in credit card debt. In Europe 20.5% of the population aged 65 or above are at risk of living in poverty or social exclusion. In the US 53% of US households at risk of not covering essential expenses in retirement, 36% have no retirement savings and the average household’s credit card debt stands at more than $6,800. It’s really important that we start to fix these numbers if we are to be customer focused and build sustainable banking businesses, companies and communities.

However it’s really hard to change because:

1/ Helping customers doesn’t come naturally to many banks whose business models are focussed on NII and fees

2/ Spending money is generally really good fun, whilst saving money, budgetting and growing wealth is generally really boring and really hard. Because of this we are up against some pretty tough mental conditioning, which is very difficult to re-wire.

Research over the last 10 years into the brain, the mind and human potential has brought about a new understanding about the role and function of the human brain. Through today’s understanding of neuroplasticity we have begun to understand not only how incredibly powerful the brain is but also how it is possible to reprogram it.

A particularly useful line of research into the power of the brain concerns placebos. Many of us respond very well to placebos and create our own pharmacy of chemicals that mirror what we think we are getting. Indeed, three quarters of people who receive placebos for mental illness respond as well as those actually taking an anti-depressant. We get similar results for anti inflammatories; people can make their own anti-inflammatories, as they put their belief in themselves until they make it real. The sugar pill represents a potential, that people emotionally embrace with such enthusiasm and intention that takes the brain and body out of the past and into a future reality. As they take the pill every day, they are reminded that they are choosing and living in a new future. As we combine how we think and how we feel, we are able to create a new state of being. As the greatest chemistry factory on the planet we are the placebo and have enormous innate ability to take responsibility for ourselves and our health.

In parallel many service models are collapsing. 40 years ago we went to the doctor, gave them our symptoms and largely signed up to whatever they suggested. Now we take the diagnosis, whip out our mobiles, study the condition on the internet and think about what we want to do. If the doctor doesn’t support that, we go find a doctor who supports what feels right for us. That is very exciting and exactly what I did when I was lying in hospital with a broken leg. I didn’t like what I was hearing from the surgeon so demanded to speak to his boss and kept going till I got an answer that resonated. I repeated this when I subsequently got a golden staph infection and worked with my team to come up with an answer that was very effective but diverged somewhat to the protocol they initially placed on the bed. This is very exciting, very empowering and is happening in financial health as well as physical health as people take responsibility for their lives and no longer just consume the first idea laid in front of us. Individually we are a community of some 70 trillion to 130 trillion cells, all hanging round awaiting for specific instructions and orders from us; no one else, us. We may not be able to control out external environment but we certainly get the opportunity to take full control of our own thoughts and emotions, become CEOs of our own health; physical, emotional and financial and create our world.

But knowing this isn’t enough. Much of the software in our brains has been laid down over millions of years and few know the language it’s written in. How we think, feel and act creates our personality and that personality creates our reality. By the time we’re 35, we’re no longer really thinking, largely re-running the embedded programs, answering 90% of the 70,000 thoughts we have every day with the same answers we gave them yesterday. Beliefs get laid down and rarely change, with a large degree of ignorance about where they come from or what purpose they serve us. Regardless, they are familiar and comfortable and so we hang on. “If I ignore my bills I have more money in my bank account. When I pay my bills on time I don’t get to go to the movies that weekend” Changing any of it, our thoughts, feelings and beliefs, around for example money, demands neurological change to unwind the emotional records of the past.

This is why doing what we do at Moroku becomes incredibly important and powerful. A system of intelligence, that sits between the transaction paltforms and the user experience to guide customers through their money missions. The objective is to interrupt some of those negative emotions and support better habits, that over time re-wire the brain.

Most banks around the world agree they need to have a compelling digital channel offering. Currently this is translating to a lot of banks digging out their PFM plans originally written in the 90s – I know, I built a PFM plan in 1999 and binned it for the same reason I’m not building one now. Putting graphs and charts in front of 90% of the planet won’t change people’s beliefs about money or any of the behaviours we’re trying to shift. PFMs won’t work at the emotional level to unwind the records of the past and have any capacity to break free of the beliefs around money and permit the perception of a new future. In fact they may indeed just do the reverse, presenting and pervading the past: its hard complex and only people good at maths can be good at it.

Money is a great stressor and when we live by the hormones of stress and the associated emotions we get a rush of chemicals that make it very difficult for us to determine the difference between what’s real and what we’re making up in our head. At an unconscious level we often struggle to differentiate between an experience that is causing the emotion and the emotion that we are fabricating by thought alone. When this happens all sorts of feelings come to the fore: anger, frustration, impatience, fear, hopelessness, powerlessness and depression. Millions of years of evolution have trained us this way as it used to be pretty handy. If there was a predator out “there” we get focussed on the predator, convince ourselves that we’re about to get eaten and run away very quickly. The problem with this reaction is that we feel very separate from possibility, expecting the worse outcome, selecting the worst outcome. “We’re about to get eaten so run away very fast and here’s some adrenalin to kick you on your way” The problem with that is that the hormones of stress almost always force us to select the worst case scenario, which we come to embrace. This pattern gets laid down over and over again and ends up becoming who we are.

This is a massive problem with banking as we default to old habits, thoughts and beliefs that reaffirm old habits, responding to the same experiences with the same emotions, thoughts and responses time and again. If we do that for 10 or 20 years our brains get hard wired into fixed patterns and to step out of that is very difficult. If we want people to change the way they think and feel about money in order to get them to act differently we must change the emotional context within which they experience money, creating new feelings that permit them to change their thoughts and over time create new habits and the boundaries of their beliefs.

This is why the global gamification market size was valued at USD 6.33 billion in 2019 and is projected to reach USD 37 billion by 2027, exhibiting a CAGR of 24.8%.

By rewarding and recognising great banking behaviours, like paying off credit cards on time, saving for home deposits, building wealth and creating financial plans we begin to create new emotional experiences around banking, taking away the boredom and pain of doing these things, create better customers and grow sustainable, liquidity based banking ecosystems.

Even if you didn’t commit the whole bank to this idea you’d at least run an experiment.