The predominant banking model has favoured scale over satisfaction

Since the dawn of banking time, customers and bank staff alike, were presented a convenient method of viewing their balance sheet and transaction history, little of which has fundamentally changed over time. Customer name , a summary position, a list of transactions and a capability to move money, pay bills and the like. Make it easy. Make it convenient.

The model has largely worked. Since the advent of the public internet in the late 1990s digital banking has made banking and payments more convenient, more 24*7, from anywhere. Whilst startups and technology companies have increased the access to niche or underserved markets with new assets and payment types, e.g. crypto, the predominant business model for retail banking in the world has remain unchanged: one based in Net Interest Income (NII) and convenience. The main source of revenue for banks is to acquire Cash from deposits and wholesale funding sources by paying them an interest rate “C” and then lend that to borrowers at a higher interest rate “Li” , making Net Interest Income “NII” between the two.

Li-Ci=NII

NII is sometimes also referred to as Net Interest Margin NIM. Interest rate, either Li or Ci, is a function of risk. The less risky the party, bank or borrower, the lower their cost of funds, i.e. interest rate.

This model favours scale. A bigger balance sheet favours better price, brand and customer acquisition costs whilst computing should provide unlimited scale and an associated decreasing cost to serve. The unit economics get better with scale.

This is born out by the numbers. In May 2020, mutual bank satisfaction levels hit a high 89.2%, while the four majors lagged behind at 77.2%. Despite the fact that customer satisfaction levels by the smaller banks, credit unions and mutuals, is higher than the main banks, the power of scale continues to drive headline performance in banking.

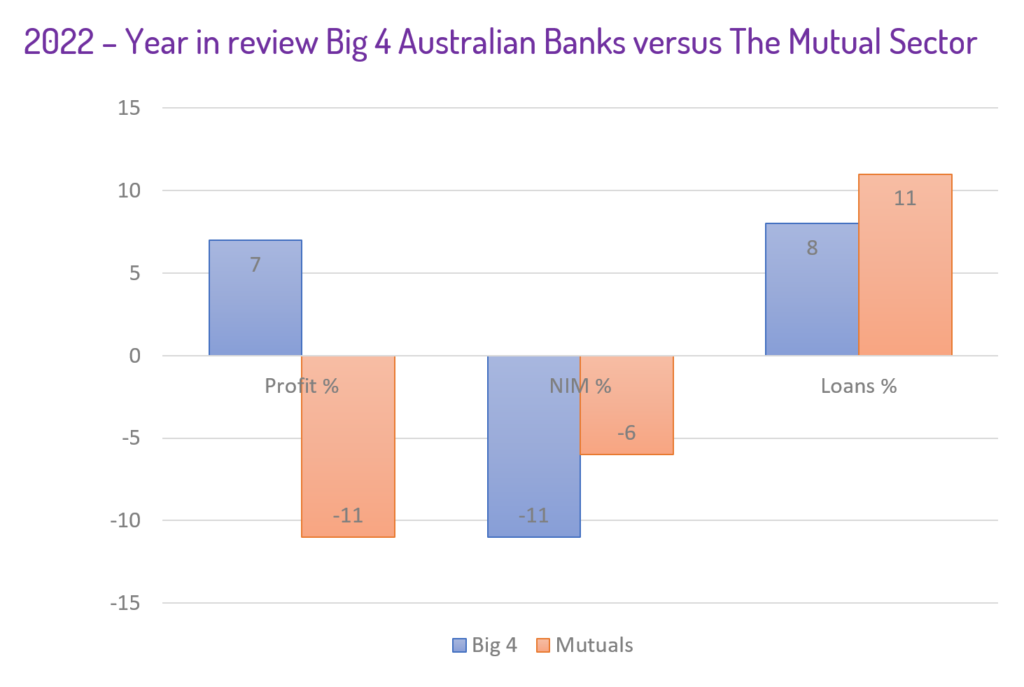

In 2022 the big four Australian banks grew their cash earnings in 2022 by 7% whilst the credit unions fell by 11% as the bigger banks grew their lending volume at a rate 37.5% higher than the mutuals. Much of this efficiency and effectiveness comes down to an operating model built on digital and the experience, with the mutual sector unable to cash in on their customer satisfaction and NII advantage. The big banks continue to outgrow the smaller players, competing on the same model: NII and convenience. Size wins. From every $1 revenue earned, a mutual bank retains after operational costs on average only 20 cents vis-à-vis major banks’ 50 cents. On an asset base 50-200 smaller than the big banks’, your annual investment budget as a larger mutual does not exceed $10-30 million compared to major banks’ $1-2 billion.

Yet there are increasing signs of diseconomies of scale. TNex in Vietnam were able to achieve unit economics that many larger banks could only dream of . By building infrastructure that was digital and core native, not only could they achieve great efficiencies, but also improve customer satisfaction by being focussed on customer success. Larger banks, struggling with spaghetti legacy infrastructure and groaning political cultures that fail to grasp growth mindset, see escalating costs and leaky sales funnels.

If smaller banks are going to persist and thrive they need to change the underlying business model to one that allows them to take advantage of their customer satisfaction advantage and deliver this through a digital platform that allows them to scale. Without scale they will be unable to invest in cyber security, user experience, risk and data technologies for them to exist and escape regulator intervention.

Moroku proposes such a business model and supporting digital platform. The business model is based on share of wallet; engaging and rewarding customers across a full range of products, including loans but also deposits, payments and investments such that they can grow their capital platform. Customer success is recognised and rewarded , building empathy and trust based on the high trust relationship model, introduced by Steven Covey. To do this a number of KPIs need to be added to the performance dashboard of the organisation:

- Customer Success – The number of customers as a percentage of overall customers who pay off their loans in a given accounting period.

- Main Financial Institution – The % of customers whose wages are deposited with the organisation

- Average number of products – the total number of products used in a month/total number of customers. This is a proxy for wallet share

From there a digital experience that promotes strong money habits in line with the organisation’s scale objectives is required. Such a digital experience is presented by Moroku:

- A lightweight, mobile and internet banking solution, configured to support multiple brand needs across multiple countries and therefore payment systems without any customisation.

- An organisation shall choose and change the components it wants, including local language, brand, core banking and payment system nuances and that once chosen, it’s version of the app, on web and mobile, whenever generated or updated would pick up these configurations.

- Such a solution is competitive with that provided by the big banks

- An increasing range of content, money tools, reward and notifications are increasingly revealed in support of the revised business model of customer success, through the implementation of the Odyssey domain model..