It is well known that humans have a range of cognitive biases that get in the way of our logic and reason. These biases are particularly acute when it comes to the psychology of money and how difficult it is to be great with our money and do the right thing. Treating financial services as a game is the most transformational opportunity available to financial services executives looking for an opportunity to out compete the market. When we put our customer’s success at the heart of the product design process we unveil fabulous opportunities to win. When we recognise their need for fun, reward and engagement over more cognitive distress we make further ground.

With more and more customers spending time within mobile games, adding game mechanics, elements and design patterns to banking experiences to make them more appealing, engaging, and fun, is on the rise. Game elements embedded into the user journey make routine tasks engaging and fun. Defining customer journeys within the construct of player maps go even further by making the engagement strategic and contextual. Together, game mechanics placed within game design convert the boring financial task from distressing to-do list into an engaging activity where players get about their work within the construct of games, leagues, missions and challenges as they gain skills and level up.

Key areas to leverage these notions in the banking industry include:

- Encourage savings: Savings is the easiest functions to gamify and perhaps the most important. Large segments of the population have no cash reserves for emergencies and live pay check to pay check. This represents the greatest area for financial institutions to help in regards to financial wellness . One can allow users to set savings targets and reward them to complete the goals and build savings habits

- Encourage better financial management: Apps with financial limits and budgeting systems to assist users in developing personal financial plans, tracking spending, and adhering to a budget. Yet most of these are boring and provide no insight. So what if I spend 17% of my money on utilities? what’s the insight? What’s good? What’s bad? What’s better? There is much to improve in this area and you can see these ideas with Money Matters

- Increase financial literacy: Incorporation of content, podcasts and short videos that explain complex financial concepts in an engaging way at the right time in their journey

- Paying off loans. Getting a loan is one thing, paying it off another, requiring discipline and systems to stay on top of it and get it done. There are many tricks that need to be incorporated and which are often daunting. Rewarding , recognising and nudging good behaviour and loyalty can be a win:win

- Training and motivating teams: Learning can be made more meaningful by using real-life simulators with gamified design and mechanics

- Managing insurance risk: Application of game design to shape user behaviour. Scores, bonuses, and other fun features help users follow insurance contract terms better

- Promoting sustainability: Tracking sustainability impact of purchasing decisions at an individual and community level to support sustainability goals

- Building community: Recognising that people aren’t alone but that we are operating together can overcome notions of loneliness and create a community feeling.

Whilst gamification had an early spurt, then went out of favour it is back on the priority list and will continue to have a significant impact on how we motivate people to complete difficult tasks and achieve their goals. Gamification has the potential to influence a wide range of emerging fintech ideas in the future.

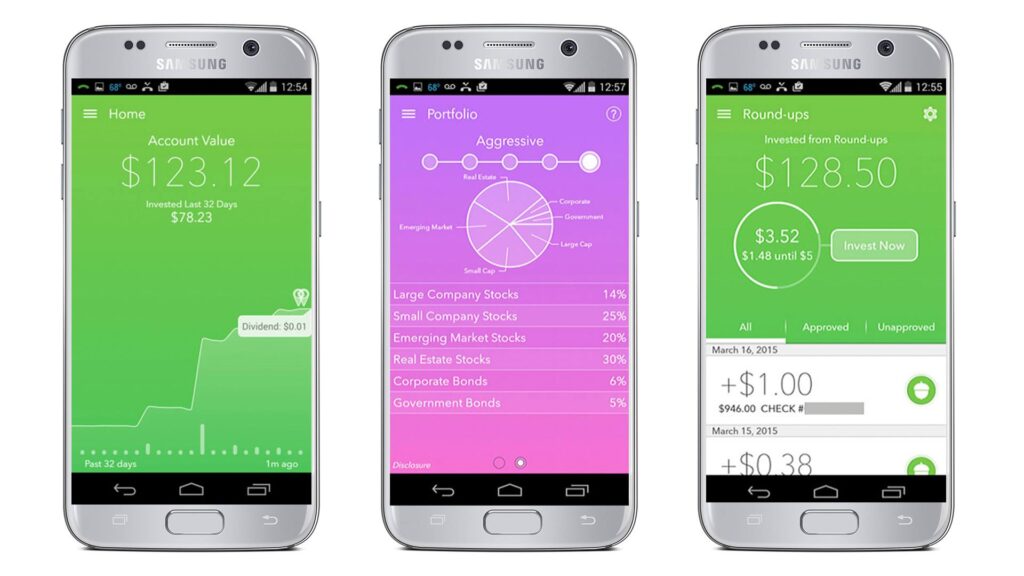

Gamification and personalization: how Acorns achieves 99% retention

Can you imagine mobile user retention of 99%? For most mobile marketers and developers, that’s fantasy land. Most who are struggling to boost engagement and retention have 10-20% user retention after a month if they’re lucky.

Acorns uses segmentation, gamification, and a sophisticated messaging and CRM strategy to fully engage every user and achieve almost unheard-of user retention numbers.

They

- Give users tiny hits of dopamine to boost retention

- Manage price

- Deliver segmentation within the app experience

- Pay attention to the leaky bucket

- Treat individuals individually

- Provide real-time feedback

- Map customer journeys granularly

Other examples include

- Kuvera gamified the mutual fund investments by offering value-added services like tax harvesting, family account planning through loyalty coins

- Built on the entire life cycle of money management, Birdfin, enables parents to schedule tasks for their kids and offers Digital currency in return

- On the occasion of Diwali in 2019, Google Pay came up with a gamification model according to which the users needed to collect stamps by scanning festive items or by transferring money/making payments

Moroku’s vision is of a world where everyone is great with their money. To do that, financial services need to be engaging, fun and social. When service is this way, people pay attention, become curious, overcome challenges, grow skills, and embark on a journey to mastery. Characterised by games and social, customer engagement, of all ages and backgrounds, is being redefined. Customers want to have fun, take on challenges, be recognised, grow and share. Moroku’s Odyssey platform and processes create engaging financial services experiences for banks and FinTechs that empower and engage customers and helps them all to become great with money.