Digital Experience Platforms

The global Digital Banking Platforms market size is expected to grow USD 8.2 billion to USD 13.9 billion by 2026.

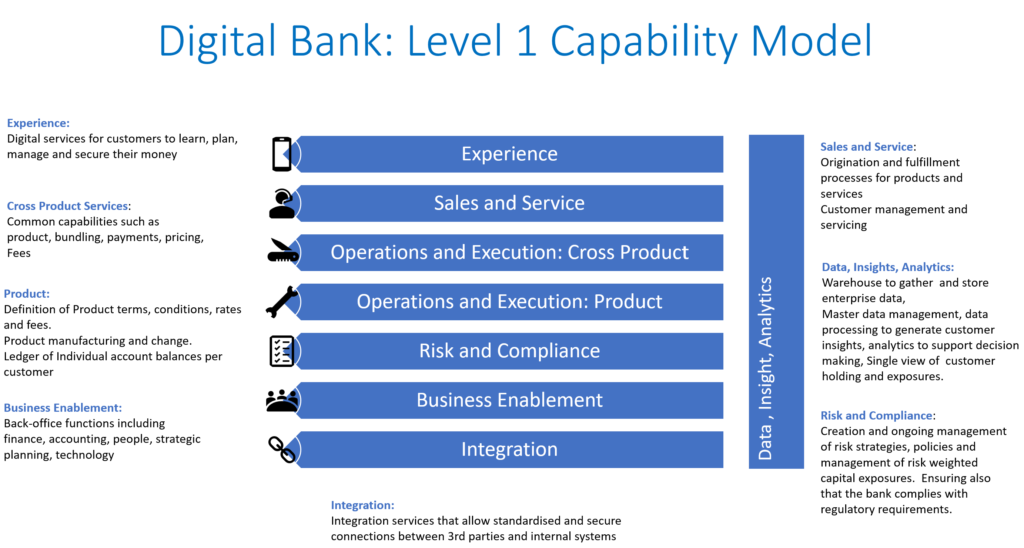

The Moroku Banking Capability Model breaks this market across eight first level capabilities. The Experience capability sits at the top to provide digital services for customers to learn, plan, manage and secure their money.

The Digital Experience Platform (DEP) breaks down into the following level 2 capabilities to drive engagement and loyalty.

Anonymised Identity

As a cloud-based architecture, the digital experience needs a method of understanding who a player is in a way that is anonymised but mapped to a customer behind the firewall. This ensures player state can be managed as they journey their money terrain whilst the platform remains indifferent to cyber theft attack.

Integration Service

The DEP needs to receive and create transaction events with the level 1 operations and execution capability of the bank such as account opening, player lifecycle and payments. In order to act upon events the DEP needs to know about them. This occurs through the Integration Service that identifies the key set of engagement events and notifies the DEP of them in relation to the anonymised identity. In return the DEP passes on instruction information such as account opening , payment size and timings. This facet of the DEP can provide some hope and delay for banks struggling to risk core transformations .

Event Harness

Experience platforms are event driven to ensure that they are contextual. It is no longer sufficient to map out standard, linear, one size fits all products and services that customers have to figure out how to use. Data driven events will determine and increasingly personalise content and services for customers based on their context – who is the customer, where are they in their journey individually and in context to their relationship with the bank? How long have they been here and where are they up to?

With no shortage of data from open banking, customer histories and third parties, the race is on to map these within the terrain of a customer’s financial life, prioritising the hyper-personalised customer experience.

Driven by Amazon and Netflix, basic personalised insights will become table stakes for financial institutions by the end of 2022. As Customers are starting to expect a higher level of personal interactions from their bank, data-driven personalisation can make it happen.

Consumers and small business owners expect their banks to go beyond traditional account offerings and provide reliable tools and resources to help them understand and improve their financial health. This includes giving them a lightning-fast overview of where their money is and how it’s being used, available at their fingertips,” Chase’s chief product officer, Rohan Amin, recently wrote. Consumers and small-business owners will demand more personalisation, he added, which will lead to “hyper-personalised features that deliver tailored experiences based on real-time dynamic signals”

Whilst AI has been focussed on ChatBots and credit risk to date, digital intelligence will increasingly be used to hyper-personalise the experience and drive the segment of one, fine tuning the rules by which events are created and reacted to. A host of outcomes will be prompted through notifications and other mobile first style game mechanics as customers journey through the engagement loop within the guard rails of the money roller coaster.

The Event Harness operates as the black box for the multi-dimensional player journey, providing a stackable if this, then that nudge engine that triggers win states and other boundaries between the cogs of the engagement loop.

Organised and Managed Money

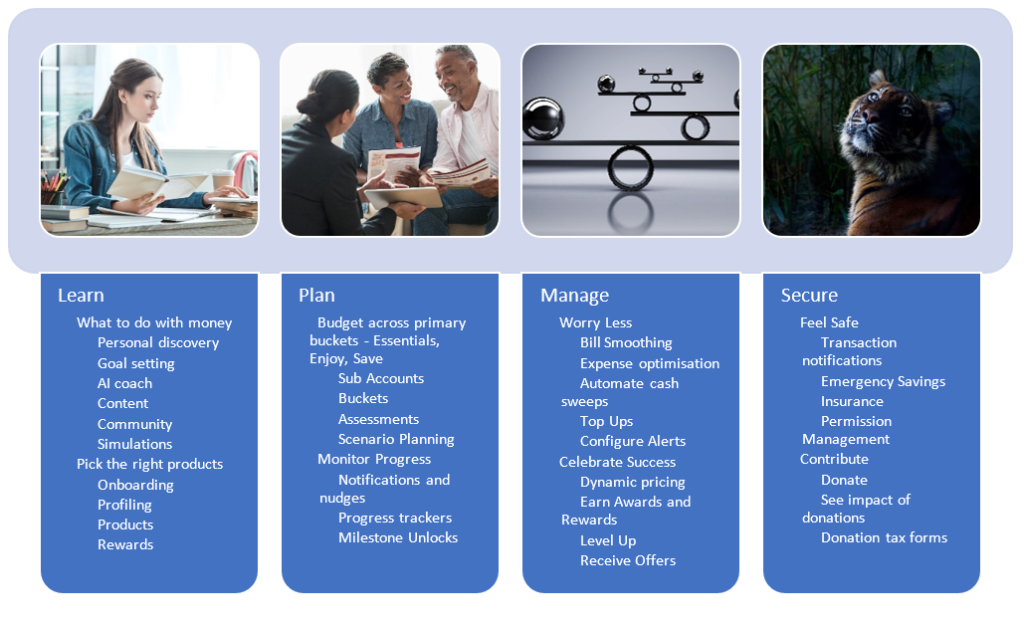

Ultimately the DEP exists to provide digital services for customers to learn, plan, manage and secure their money.

Money management is no longer about getting your money into one or more banks with some budgeting tools. These early budgeting tools presumed a level of knowledge about what to budget for and by how much. Money needs to be managed across numerous buckets such as the 70:20:10 system so customers can get organised across the various aspects of life such as essentials, enjoyment and nice to haves and their goals and savings plans.

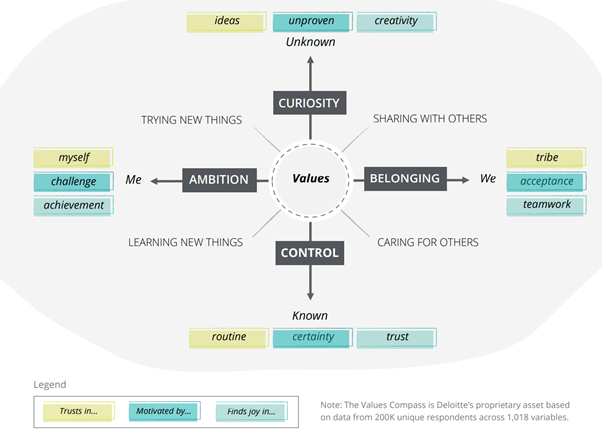

Much of this begins with a personal journey of discovery about how we feel with our money and the beliefs and values we have and which may or may not be productive. Deloitte’s Value Compass is a very useful lens by which to think about understanding what customers care for and how this context and insight can guide their money journey.

Whilst financial literacy has failed, bite sized and contextually relevant information and links at the right time will become fashionable in 2022, rewarding customers not only for their money work but their learning and development work on their way there.

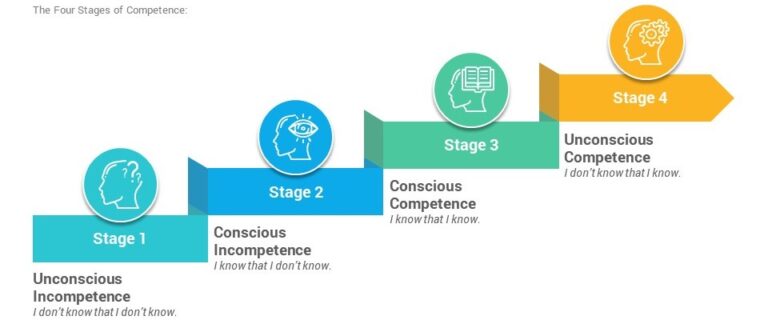

As we build out our data driven knowledge of where the customer is within their money journey, we can begin overlaying models such as the four stages of learning. Such models allow the platform to determine when the right moments are to introduce automatic sweepings once the customer has demonstrated the value a particular skill l, has formed a habit around it and has the confidence to let go and hand control of their money systems to the machine and move into quadrant 4.

The DEP contains the money systems and subsystems within it and is configurable by market segment.

Growth and Winning

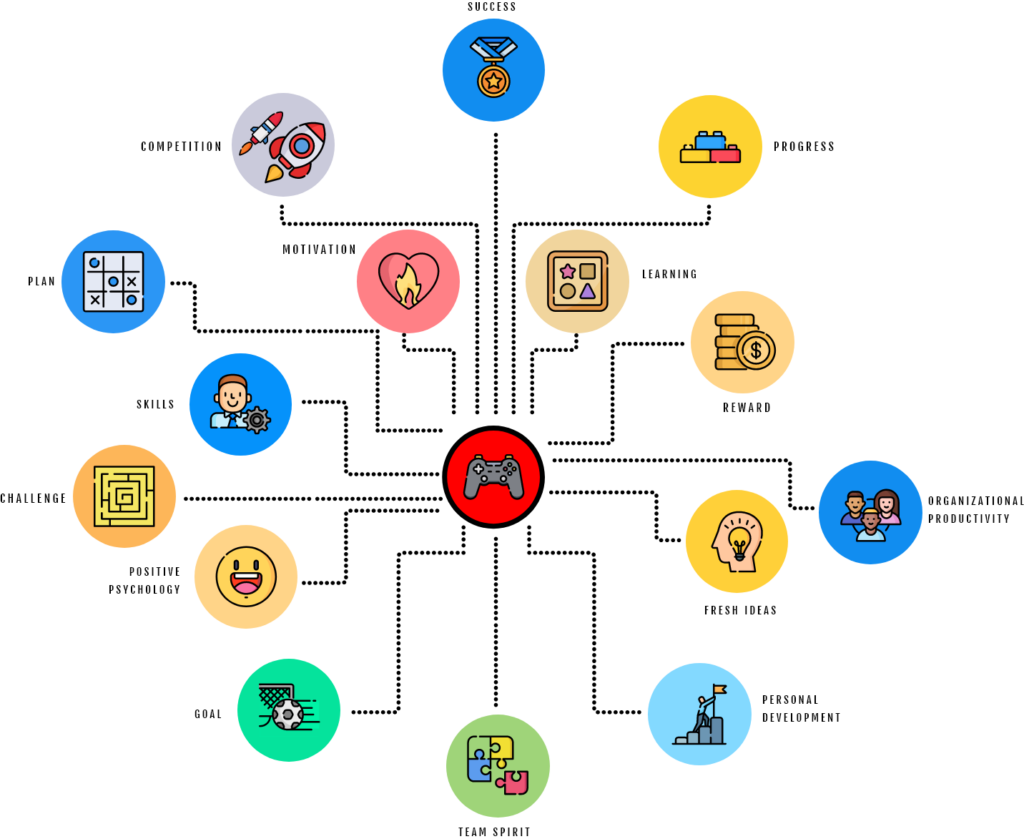

With the events harness and money systems in place, journeys are organised as a game to drive engagement. From childhood learning to war games, from lions in the jungle to humans, from Snakes and Ladders to Fortnite, games proliferate across the animal kingdom to build skills, have fun and win.

Whilst ease of use got us to where we are in digital experiences, fun to use will define the future of experiences. As digital becomes consuming we are at a tipping point where Gen-Z folk are in their late 30’s early 40’s, have grown up as video gamers. They are consuming and creating this new digital world through an adult/gamer lens and expectation set. Jakobs law states that users spend most of their time on other sites and apps. This means that users prefer your site/app to work the same way as all the other sites they already know and have arrived at your app from. In 2022, banks have to assume that players have just been playing a mobile video game with dopamine pumps firing and ready for their next mission, challenge, boss fight and level up. This demands that the DEP is constructed around the game metaphor.

The DEP will be required to support the incorporation of a range of game mechanics that can be triggered from game dynamics that are set up with the Events Harness. These will cover a host of extrinsic rewards, allowing customers to convert points to prizes as well as intrinsic awards that acknowledge win states and unlocks.

Personalised Pricing and Plans

Industrial Age marketing was premised on the 4 P’s. The Brand was an image, badge, promise, trustmark or “word in the mind.” From here the marketing machine pushed marketing content around the famous “Four P’s” of marketing – having the right product, being in the right place with the optimal price and effective (one way) promotion.

As experiences become digitised and connected, customers are demanding – and smart businesses are providing – technology experiences centred on the preferences of individuals. In the era of big data, hyper-personalised objects are creating a ‘Market of One’. This is only possible by data being king, especially in a world that will be increasingly driven by AI which uses data to develop its algorithms. The likes of Amazon understand that the true standard for hyper-personalisation is interacting one-to-one with individuals rather than segments, and that to anticipate any individual’s desires requires deep customer insight derived from analysing granular data.

This requires the DEP to build an increasingly deeper opinion about the customer, mapping out where they have been on their journey, understanding that in reference to the very many customers that have followed a similar path and where they may likely go next. This will allow the platform to begin treating them like an individual.

This platform can then be used to recognise customer share of wallet and tenure and offer up pricing and plans that reflect that loyalty and effort and guide them to staying longer and using more products, becoming stickier. This will allow micro moments of reward provided at regular intervals compared to the 4 levels of an airline reward program that have been notorious at not treating customers in segments of one. Engagement will supplant basic transactions as the key determinant of loyalty.

Conclusion

Banks are under pressure to be more innovative to serve customers better or give up share to those that do. New brand promises that are oriented around customer success and deliver that through digital experience platforms will be the segment leaders. These digital experience platforms will intelligently understand where the customer is on their journey and provide them with the resignation, encouragement and reward that they yearn for in the very often lonely world of money.

As banks give attention to this they will target investments in Digital Experience Platforms that have the above attributes to compete within the new digital trends.

Moroku has the platform and design processes for digital challengers that are ready. Is that you ?