Earlier and reduced onboarding friction coupled with better data aggregation across the lending mission presents real opportunity for lenders and borrowers facing some of the most difficult economic challenges in decades. With lots of anxiety, the hunt is on to provide value and help customers feel better about their money, their decisions and their home.

Moroku works alongside our customers and origination providers to use the Odyssey player maps to define the lending mission CX, lay out the task at hand, rewarding effort and loyalty across time space and motion then integrate Odyssey to deliver the moments.

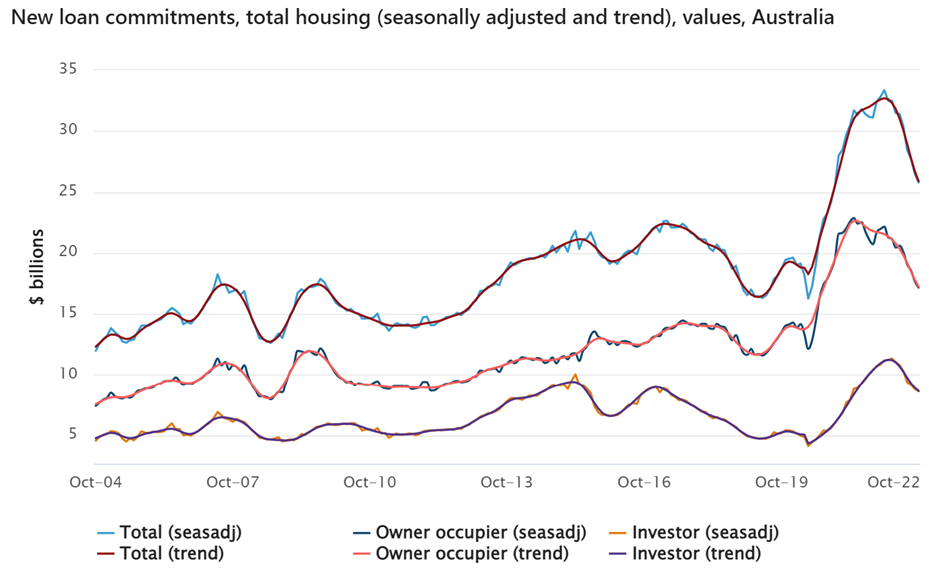

Home loan volumes drop as customers go analog and non bank lenders file for bankruptcy

Interest rate rises in Australia are impacting home loan volumes, falling 4% in the first quarter of the FY23 and picking up speed in the December quarter. Shrinking volumes are hurting non-bank lenders the most, falling to their lowest market share since 2020 as customers go analog as the broker channel climbs to 68% of the market.

New Zealand may now be in “phase two” of the property market downturn, Corelogic says, as rising interest rates could add $12,000 a year to the cost of a $500,000 home loan, a 2.4% increase. As New Zealand’s housing market continues to plummet, the owners of one home have opted to throw in a free Tesla to try to entice buyers. The overall volume of houses sold in October has dropped dramatically: down 34.7% compared with last year, from 7,486 to 4,892.To protect themselves the majors are tightening their risk criteria, passing on some of the rate change to borrowers whilst keeping some for themselves and increasing lenders mortgage insurance (LMI).

In the UK buyer demand fell 44% year-on-year in October, while sales volumes were down 28% compared to a year earlier. The central bank said mortgage approvals were down 10% from the previous month, as demand for rental homes in Britain rose in October as prospective first-time buyers put off purchases amid the surge in mortgage rates. Robert Gardner, chief economist at Nationwide, told BBC Radio 4’s Today Programme that the typical mortgage payment compared to average earnings in London is up at 75 per cent, well above the previous peak before the financial crisis. Consumer savings is almost double the pre-pandemic level with consumer credit down 42% from £1.2bn in August to £700mn .

In the US The US mortgage industry is seeing its first lenders go out of business after a sudden spike in lending rates, and the wave of failures that’s coming could be the worst since the housing bubble burst about 15 years ago. Mortgage rates that have doubled this year are sidelining potential buyers and causing sellers to pull back on new listings with pending home sales having fallen for five months in a row. Mortgage applications are 41% lower than one year ago. Again it’s impacting non-bank lenders hard. Rocket, one of the largest mortgage lenders in the US, reported $25.6 billion in loan-origination volume for the three months through September, down from $34.5 billion in the previous three months and $88 billion a year earlier, with Net Income plunging 93% to $96 million in the third quarter. The company is dealing with ‘challenging market conditions,’ the CEO said. Reverse Mortgage Funding, a home lender backed by Starwood Capital Group, filed for Chapter 11 bankruptcy this week. Layoffs have been widespread. Opendoor Technologies Inc., which pioneered a data-driven spin on home-flipping known as iBuying, laid off about 18% of its workforce and wrote down the value of its property holdings by $573 million. Brokerage Redfin Corp. went through two rounds of layoffs and shuttered its iBuying business, while competitor Compass Inc. also made deep cuts to its technology teams in a quest for profitability.

Whilst there will be some staff retrenchment, 2 sets of eyes on loan applications, improved automation and digitisation is called for

Customers are getting harder to acquire, nurture through the process and retain. There are less of them and as mobile natives, customers need to do it all with their index fingers and thumbs, during occasional moments of waiting during their day or between Netflix episodes. With rising interest rates, fluctuating property prices, reduced borrowing power, an increasing cost of living and a Cambrian explosion in provider offerings, there is a lot to navigate. This is causing more customers to back out of digital, and head to the broker, with the broker channel, now responsible for 68% of the market, unless this complexity can be simplified through the digital journey. An increasingly popular way of doing this is through the application of game theory to not only guide the customer but also do so with fun and reward as they journey across time, space and motion using the engagement triad.

Some in the industry will be facing the Qantas baggage handler dilemma. During the pandemic the national carrier furloughed many of their staff. When they wanted to turn the tap back on, many of these folk had found other jobs and didn’t want to return to the airline. This made it very difficult for the airline to satisfy the pent-up demand to jump on a plane. Whilst the downturn in mortgage volumes would appear to see many lending departments sitting on their hands, a case for redundancy, there is good reason in using these people to work on Kaizen Improvements, embed Better As Usual cultures, be ready for the upturn and start being more competitive today.

Under these conditions many boards will be forced to cut operations as growth and income both drop. In Australia, as perhaps in other markets, the big banks have increased market share by 4.38% to 60.77%. as their cost of money is lower than their competitors, enabling them to offer more competitive rates. Open Banking was introduced by the regulators to reduce the monopoly of the big banks in the lending arena. This experiment remains a work in progress. Under these market conditions more will need to be done.

Spotifying Lending to Deliver Engagement and Unlock Value with Moroku

Outside and within these market leaders, options are necessarily being evaluated. More can be done. Customers want homes not loans. They want good prices, flexibility, speed, options and knowledge about how to evaluate those options.

Lender turnaround times, the average number of days until formal approval, is still averaging 17.2 days. This is extraordinarily long given the origination technologies available pointing to very many opportunities to revisit risk appetite and decisioning policies whilst protecting the lender to get customers offers faster, especially as speed to approval is a key determinant in a borrower deciding who to borrow from. Advanced origination technologies like nCino and Cloudcase can certainly help by streamlining the process, bringing the data into the engine and getting to offer. Moroku can help by engaging customers earlier in the process, allowing the lender to get ahead of the queue, rewarding the customer through the application process and making something arduous into something fun and continuing the engagement post origination, to nurture them through following levels.

Pricing needs to be competitive to win and is in the hands of finance and risk operations within the lender. These operations determine the source and volume of capital to be lent, the type of loans to be made available to whom at what price and terms, a major driver of complexity. If the journey is hyper-personalised, as is the strategy and through the implementation of Moroku Odyssey, pricing too can be personalised based on loyalty and engagement levers as the business model is Spotified and oriented towards engagement as a priority.

Getting offers to customers and the loans originated into the core systems is the responsibility of the loan origination systems. Credit policy determines what documentation is required from the customer for each loan type, where to get it, how to process and store it, how to decide, get the offer to the customer, get them to sign the terms and get them the money. The origination platforms then implement these and are responsible for delivering the flexibility, speed and options to the customer subject to competitive credit decisioning policies. Having customers into their individual Moroku Odyssey leagues in advance or during this process can help enormously with keeping them engaged and staying in the process.

Some Earth Shakingly Things

Bank and lending technology spend is on the rise. JP Morgan Chase bullishly announced it plans to increase its annual technology budget to $12 billion. Yet as the Forbes article points out, “It’s not just about how much you spend—it’s also about what you spend it on. Most banks are simply not looking to do “earth shakingly” things with IT“

Outside of pricing and origination however there remains even much that can be done such that customers feel value when we change the design paradigm, shifting the pattern from ease of use to fun to use. The journey to property ownership is long and most often never-ending. From exploring choices as a first home buyer, through changing economic times and loan terms, through buying, selling, renovating, investing, downsizing, retiring and succession, there is much for customers to navigate. It is here, through this navigation, that much of the value in a lender is untapped. There are volumes of expertise within banks, credit unions and non-bank lenders, usually locked away in vaults within credit, finance and risk or uploaded by the truck load onto the company’s website for customers to trawl through. Moroku Odyssey integrates into the digital fabric to lay out this journey and deliver an end to end customer experience as customers grow with their money and see the value in the lender as someone who provides them with more than a loan.

With this lens, everything changes as we upack the needs of the novice all the way through to the master as they overcome challenges, build skills and habits and level up to unlock better services and product as they journey through time (loyalty), space (value) and motion (moemntum and cadence) with the lender.

Learning and growth moments are important for customers to understand the process and see value in the relationship. Lenders have troves of documents and content and have them all available on their websites. Yet customers don’t want to trawl through these. As mentioned in a previous article, in a world of Snapchat, TikTok and Twitter this is however all looking rather outdated where mobile is the digital platform of choice and the prime window within which to consume content. In this world, snackable content rules. The shortened attention span of an average internet user is about 12 seconds, demanding that content is concise, and contextually relevant. Pages and pages of content don’t connect. What’s required is content that high level concepts can be understood within 12 seconds and consumable within 90 to 180 seconds. With the content prepared in this way, it needs to be placed, or unlocked by the customer at the right point in their journey. This is where the Odyssey player maps kick in. Player leagues, missions are laid out through On-Ramp including where customers unlock what content.

The maps also include the notions of missions, levels and challenges. With the lending mission there is the notoriously difficult challenge of documentation, the collection and submission of customer documents related to their purchase, assets, expenses, income and deposits. Often, attempts are made to gather these all at loan time, but often these can be collected earlier as the customer embarks on the journey so that they are ready. Open Banking has a lot to offer customers here as they begin their preparation and explore what they could buy, turning loan calculators into real time, loan exploration maps.

The economic volatility of the moment is impacting lending businesses. In the face of staff layoffs and bankruptcy filings, lenders are compelled to deliver solutions that drive operational efficiency and competitiveness by reducing time to offer and deliver more customer value. Moroku Odyssey delivers customer value by taking customers on their money journey within the customer digital experience, taking them into the origination process and bringing compelling value to lenders that want to win.