Banks have been good at engaging customers when they lose whilst seeking NPS. For decades banks have been posting letters to customers notifying them of all the fail states: Overdraft notices, missed payments, failed FICO and credit scores.

Alognet is a digital banking company with a promise of driving greater lifetime value and lowering total cost of ownership. On a subsidiary website they define a notice letter as follows.

“A notice letter informs a bank’s customer about his or her account—and often explains that action is required by the customer. Financial institutions send notice letters regarding items such as a past-due payment, loan maturity, or loan default”

They go on to say that …

Email notice letters are increasingly popular at banks. Email lessens the administrative workload by providing a more efficient means of communicating with customers and documenting the receipt of notices. Notice letters play an essential role in loan file exception tracking (e.g., requesting updated financial statements or tax returns). Properly documenting the distribution of notice letters is a key component of due diligence. Once received, some customers will take immediate action, but others may not. Second notices are then generated—sometimes with a response deadline. Through the notice letter process, a financial institution’s documentation should indicate to a bank examiner that it is acting in good faith and working to clear loan file exceptions.

Its heady stuff this clearing of loan file exceptions. There is no doubt that much of banking is compliance and risk driven, creating a culture constantly on the hunt for failure. Large investments are made in systems, technologies, processes and people to seek and remedy failure. This focus and prioritisation creates a culture of compliance and a set of beliefs and values around what customers are as they “document due diligence”.

From the customers perspective it creates a set of beliefs and values around what banks are, especially when the only time they hear from them is when the customer triggers a failure event, as the bank over indexes engagement around failure.

Whilst keeping these fine systems in place, there is a significant opportunity to swing the engagement index in favour of customer success.

Despite the current systems and efforts put into managing failure, customers succeed more than they fail. Most of the time customers make payments on time and in full, stay out of overdraft, grow their credit scores, build assets, have a bit of money left over between pay cheques, upgrade their home, send their children to school or university, go on holiday, pay off their loan, beat the market, build up their pension fund, open up a trust fund or savings plan for their children and on and on and on. A life of struggle, getting stronger and stronger as they level up.

Despite all of the focus on CRM systems to provide next best offers there has been a very real and surprising lack of attention to customer success. It is surprising because if customers are rewarded for doing the right things, they are less inclined to do the wrong things. It is surprising because there is significant competitive advantage to be gained from guiding and supporting customers around an ethos of success. From a risk and compliance perspective, celebrating success and encouraging strong behaviours means less effort in documenting due diligence.

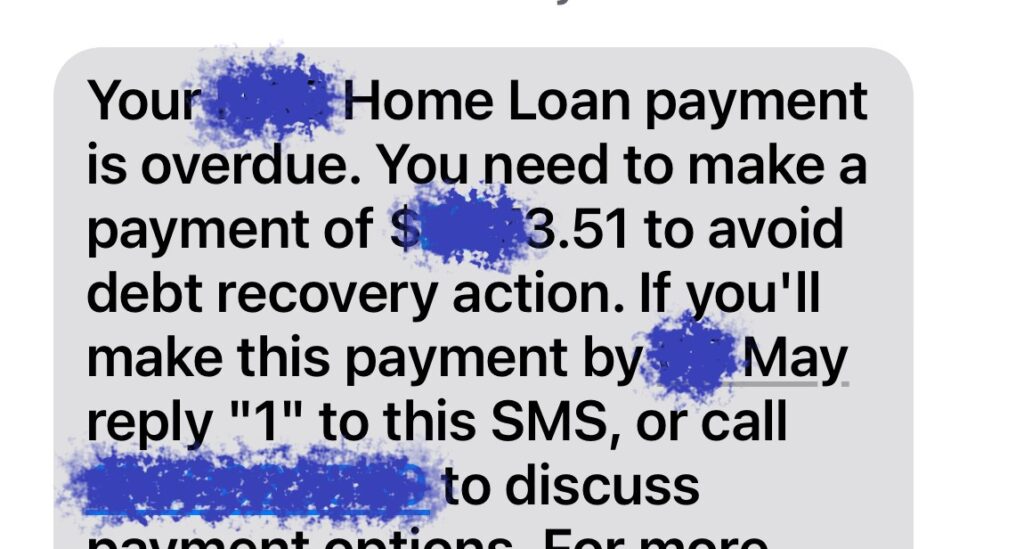

A retail lending example

Attached is an SMS sent to a retail banking customer in Australia in 2024. The bank , over indexing on failure immediatley gets on the front foot and threatens debt recovery. “Call in the dogs. If they have batons with some point bits at hand, grab them as well!”

It’s classic loan file exception management: compliance and risk driven, clear demonstration of investments made in systems, technologies, processes and people to seek and remedy customer failure. Despite the bank’s website talking about how important the customer is, their efforts are betrayed by the underlying culture of compliance and beliefs around what customers really are, as the bank over indexes engagement around failure.

How could this be different in a model of reindexing around success? The message could start with some empathy and gratitude of the work done to date. The years of toil. All of the payments made in full , on time to date. The gratitude of the bank for having the customer and so on.

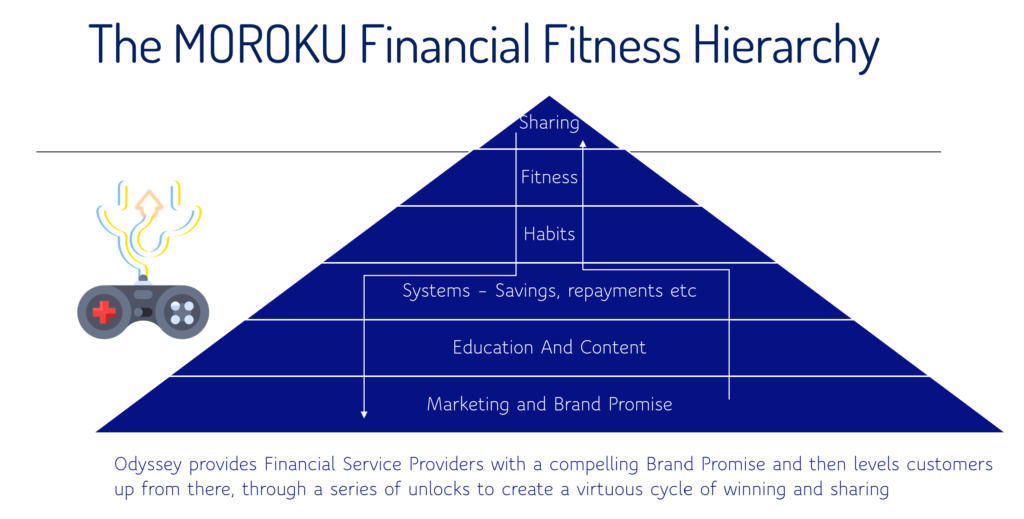

Moroku Odyssey is a set of player maps, and supporting event and content engines, for financial services institutions to celebrate success and build a brand around helping customers win with their money, creating brands that customers and staff want to be a part of. These player maps, create the initial set of algorithms to prime the AI language models to create the hyper personalised experiences banks seek.

These player maps are based on the Moroku Financial Fitness Hierarchy, that allows banks, credit unions, fintechs, wealth and insurance providers to go to market with a brand promise around customer success, delivering education and content at the right time, via content loops, that encourage customers to build strong financial management systems. These systems build habits and discipline, which, like going to the gym regularly, create financial fitness, which in turn encourages customers to share their success with friends and family.

With NPS remaining as a popular measure of institutional success, reindexing on customer success will pay off in less compliance, better NPS and stakeholder return.