Cash usage has largely been replaced by credit and debit cards other than the by the money launderers and those hanging onto a very hands on way of managing their money. Over the past couple of years BNPL has put card transactions on notice alongside their associated payment terminal businesses and their outdated technology stacks, like Tyro, where Westpac this week walked out of acquisition talks. With 54 countries now in advanced stages of rolling out Faster Payments, the edge the schemes had in terms of real time settlement is under further pressure. With near real time, person to person payments on the rise, using services such as Osko, PayID and Payto in Australia from NPP, faster payments will further erode the card schemes as the central banks begin to switch their funding and regulatory efforts away from the consumer to the point of sale. This will be facilitated by:

1/ Merchant QR Code generation, as evidenced by Oyster Card in Hong Kong

2/ Mobile banking apps, connected to faster payments, replacing virtual cards and woken up by the QR code

3/ Better APIs and 3rd Party Developer arrangements within Faster Payments

4/ Improved analytics for merchants and providers on customer trends on basket level data

Cash Replaced by Cards, Replaced by BNPL

During the busiest time of the year in retailing, UK retailers have demanded urgent intervention on interchange and scheme fees. Their cries will be ignored by the central banks in favour of replacing card rails with bank rails. In 2021, cash usage fell by half to just 15% of all transactions, while 82% were made on credit or debit cards. As they did the schemes in the UK racked in £1.3 billion just to accept card payments from customers in 2021. In Australia number is higher on a per capita basis as with the major banks making $1.7 billion of revenue from payments and credit cards. Debit cards, which generate less revenue for the card issuers and acquirers, account for the majority of transactions. As Evans & Partners analyst Matthew Wilson noted, “after growing up during the GFC and its aftermath, Gen Z doesn’t like debt, credit cards or gambling”. The same forces that have propelled BNPL growth, away from spending on credit cards in favour of smartphone apps sees the schemes under pressure.

Faster Payments gathers speed and pivots to merchant

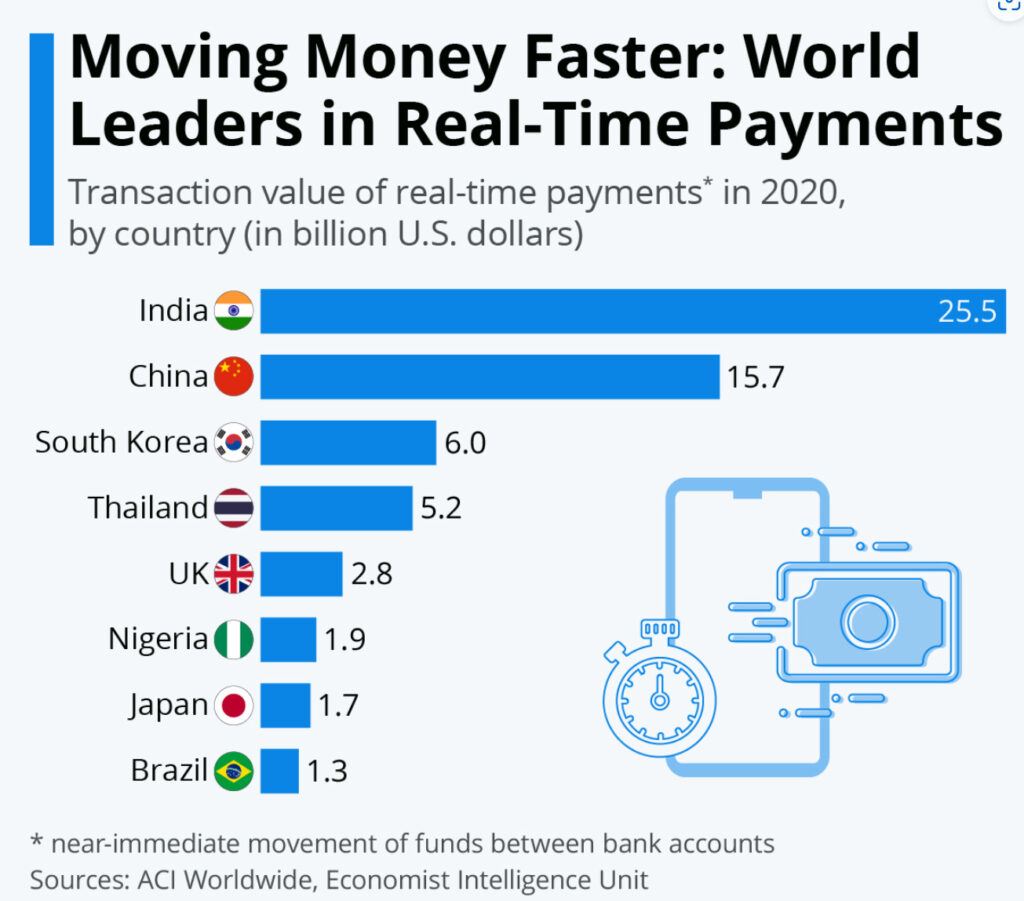

Real-time payments, sometimes called instant or Immediate Payments (IP) are the ability to transfer funds between individuals, businesses and governments, making those funds available to the payee instantly, and with instant confirmation. In 2020, a report by leader in worldwide payments, ACI Worldwide found India to be the dominant player in real time payments overtaking countries like China, South Korea, the UK, and the US. With 25.5 billion real-time payments transactions, India comfortably outpaced China’s 15.7 billion3 years ago, the number of countries rolling out Faster payments was 54. Six countries (Australia, Denmark, Poland, Romania, Singapore and Sweden) received a 4+ rating for their real-time payments systems. The U.S. and U.K. were among 31 other countries or regions with a 4 rating for their faster payments schemes. We are witnessing incumbent payments networks adding incremental features, fintechs launching customer-facing apps, and new real-time payment rails being conceptualized and developed.

Adoption is on the rise. Whilst many customers are still swapping BSB and account numbers, these are increasingly Boomers and Laggards. In a country of 26 million people, there are now close to 89 million accounts, enabled with 13 million registered PayIds able to make or receive NPP payments in Australia with one in three of all account-to-account credit transfers are occurring via the NPP, though many of these still initiated using BSB and account number, not PayID (mobile or email).

Whilst the majority of use cases for faster payments are peer to peer, bill and invoice payments, the wholly grail is the point of sale and the replacement of the card rails. This will require a combination of technology and bank business model change.

The technology is relatively easy. With PayId, enabling consumers to pay each other and set up direct debit using their email address or mobile phone number set up within mobile banking, a token sent to the smart phone requesting payment is easily done.

To remove the clunky hardware from the picture, the challenge is the seamless creation of a token by the merchant and specifically the POS and shared with the customer. This was made available in Moroku’s POS, Marrakash 6 years ago and remains ready to go. The solution also removes all the PCI challenges, a foundation for the POS Payment terminal vendors that now seem highly vulnerable and perhaps why Westpac pulled out of the Tyro deal. All of this does however require the providers of faster payments , like NPP in Australia, to find another gear ion how they make these services available to third party developers and incentivise the banks.

What’s more difficult is business model change. For years, bank executives have enjoyed may incentives for maintaining the Visa MasterCard status quo. The answer lies in the hunt for the customer. We live in an era where the search for value added services is paramount. With basket level data, such as what products were bought in what volume and price from what merchant insights for consumers and merchants explode.

As reported in the AFR, CBA’s recent integration of Paydock shines the light on where the new battlelines are being drawn. CBA will roll out the new “payments orchestration” service for business customers next year, a move that shows its desire to take on Irish-American fintech giant Stripe and wrest back valuable transaction data from buy now, pay later operators like Afterpay. CBA group executive of business banking Mike Vacy-Lyle said the bank wanted to simplify payments for customers and let them choose the services they would like to use. The bank also intends to stay in the middle of transactional data flows, which are used to assess customer risk and decide whom to lend to. “This augments our data and will lead to more lending opportunities on the back of that data,” he said. The future is not in transaction fees from card transactions. Its in knowing customers and merchants better, providing them more value. If the weather forecast says that it’s going to be 8 degrees warmer this weekend and that consumers increase their purchase of ice creams by 22.6 % that’s very helpful for accurate stock management if you sell ice-creams. Thats good value add that can generate revenue. Faster payments provides that basket level data and insight in a way the schemes can’t or wont.

The future is faster payments. It’s not crypto though those rails showed us the way forward. The call is on the providers of faster payments to unleash the fintechs and enable and incentivise their tooling into the mobile banking apps for consumers and mechants alike to streamline the experience and accelerate the adoption to replace the terminal technology that is now 50 years out of date.