The Consumer Duty Regulations in the UK are an extension of a set of developing consumer protection standards that are increasingly demanding a business model predicated on customer success and a technology stack that supports customer journeys of winning.

Consumer Duty Regulations now in force in the UK

Adding to existing law relating to consumer protection, The UK’s Financial Conduct Authority (FCA) published final guidance and a policy statement for consumer duty in July 2022. The main rules will come into force on 31 July 2023.

The regulations go beyond consumers to cover all retail clients, including SMEs and also, potentially much larger organisations such as local authorities.

The three key behaviours required of financial services firms hence forth are that they:

1️⃣ Take all reasonable steps to avoid causing foreseeable harm to customers.

2️⃣ Take all reasonable steps to enable customers to pursue their financial objectives.

3️⃣ Act in good faith

The intent here is for banks to:

- To ensure customers get the right products, use them well, are supported to make good decisions.

- By understanding the customer’s needs and characteristics, taking into account the imbalance in the relationship between them and customers (i.e. asymmetrical knowledge, bargaining power, expertise, etc).

The 3 behaviours need to be interpreted in the context of:

- The nature of the product/service offered.

- The relevant distribution chain.

- The reasonable expectations of consumers for a particular service/product

- The specific characteristics of the customers

Implications for the banking business model

Since the dawn of age, banking has been based on borrowing low and lending high, the Net Interest Income model, whereby customers are largely provided a small interest rate for their deposits and charged a larger interest rate for their borrowing. Banks effectively created a 2-sided marketplace and were able to scale this beyond their customers by accessing wholesale funding on the open markets to increase what they can lend subject to balance sheet constraints.

To a large extent, this model thrived on customer failure. The best customers never paid off their loans and greater margins and fees accrued from customers who were delinquent, vulnerable, risky, needy or otherwise disadvantaged. No wonder Jesus apparently took it upon himself to lay down a most famous protest.

And Jesus went into the temple of God, and cast out all them that sold and bought in the temple, and overthrew the tables of the money changers, and said unto them, my house shall be called the house of prayer; but ye have made it a den of thieves.

The first phase of digitisation of banking in the 90’s was based on cost to serve: reducing the cost of serving someone in the branch of about $10 to $1 via the internet. As the internet became ubiquitous through mobile, the relationship became one of convenience, being able to bank and pay conveniently and this became the marketing message – “Bank with ABC anywhere anytime through internet banking”

Since that messaging took effect in 1997, the world has moved to digital banking, with more and more people around the world turning to online banking for their financial needs. According to recent statistics, 73% of US adults, use digital banking services. In the UK, its 89%. European figures show that between 2018-2022 90 .4 % will be accessing their accounts from mobiles phones and 80 % make payments digitally too. Additionally, 35 % report an increased frequency due COVID 19 pandemic whilst 22 % switched over completely during this time period. We’re in!

The Third Phase of Digital Transformation

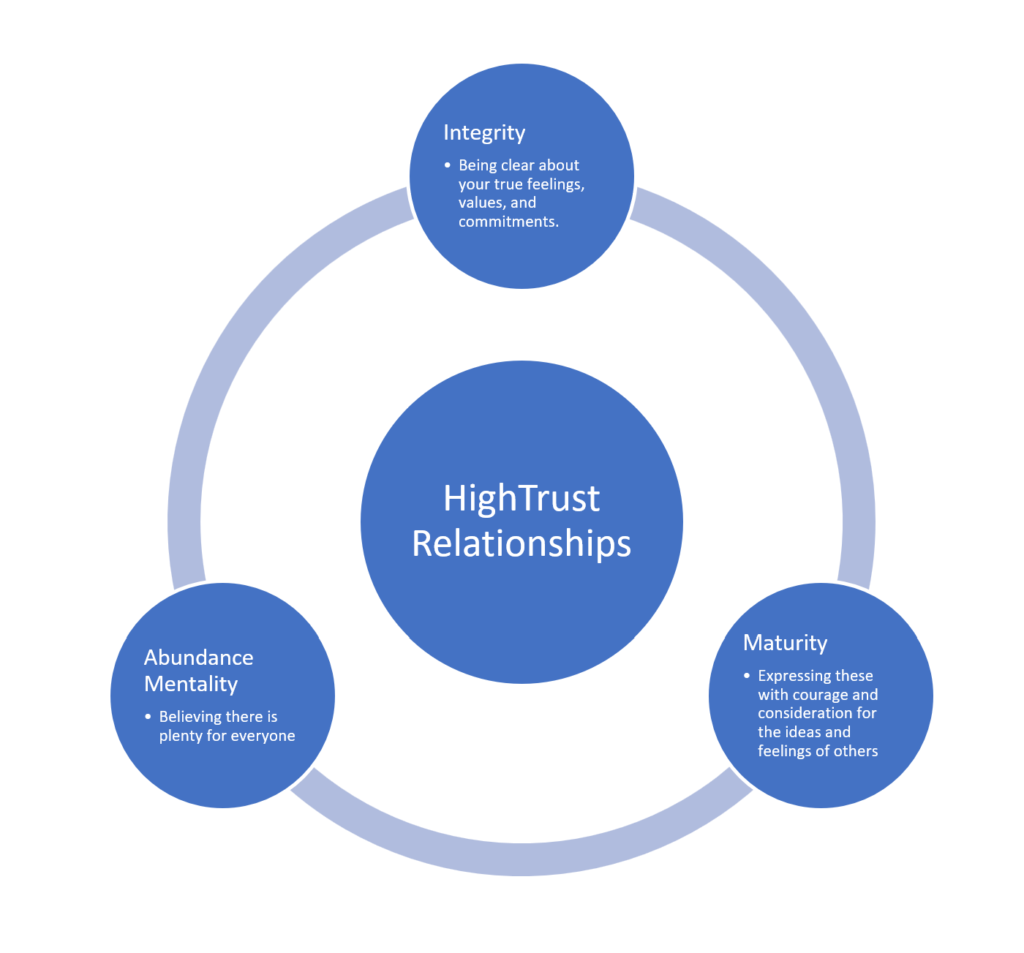

We are now in the third phase of digital transformation, one oriented around deepening the relationship as NAB Chair, Phil Chronican so eloquently puts it. The winners in digital are moving to a win-win model and are doing so ahead of the regulations. Under win-win, customer success, engagement and happiness are at the centre of the business model as a moat is built around customer loyalty, as coined by TNEX CEO Bryan Carrol who built the most successful digital bank in Asia, perhaps the world.

In Steven Covey’s “7 Habits of Highly Effective People”, win-win sees life as a cooperative arena, not a competitive “I win, you lose”” one. Win-win means solutions are mutually beneficial and satisfying. To realise win-win, you must be empathic and confident, considerate and brave. That balance between courage and consideration is the essence of real maturity and is fundamental to win-win. Success is centred on the notion of establishing high trust relationships between the parties, which can be built by consistently exhibiting three vital character traits.

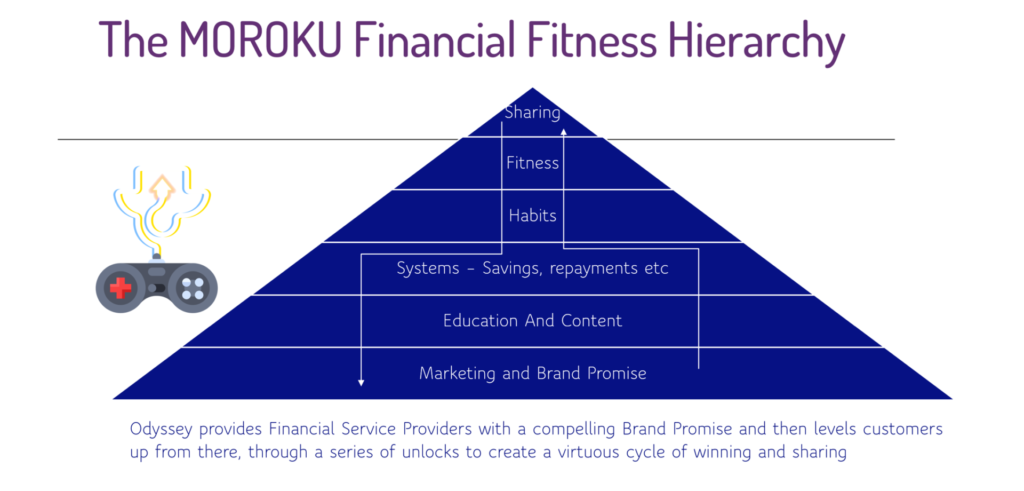

Translating this to a new banking business model, one predicated on customer success, can be achieved through the lens of the Moroku Financial Fitness Hierarchy.

The model begins with a brand promise that is dedicated to customer success, helping customers build wealth, pay off their debts, have money left over between each pay cycle and thriving with their money. The customer journey starts by recognising that doing so is not easy for most people, that it’s tough lonely work for many, requiring discipline and awareness and builds content around that.

From here products and services, which Moroku collectively calls money systems, are construed, and placed at critical moments on the journey that customers unlock as they build up their systems to remove the cognitive overload and start automating their money, in advance of their cognitive biases taking over.

As these systems take over, customers build strong habits that in turn create financial fitness that is shared and evidenced by friends and family as to the great job the financial institution is doing to serve them. Abundance becomes a mindset of the financial institution and the customer.

The rewards for the win-win bank can be significant. New clients brought in not only by the promise, but the products and success of others, more effective customer engagement and insights, more automation, value-added services and a holistic omnichannel approach to digitisation.

By getting personal, building empathy and delivering customer journeys built around success, high trust relationships can be built on shared values.

Implications for the Technology Stack

In addition to establishing win-win, Steven Covey implores us to begin with the end in mind as the 2nd habit and is again highlighted as key to success by Phil Chronican. As well as a clear target win state, this involves defining clear measures of success and a plan to achieve them.

Again, there is alignment with the FCA that has identified more that firms can be doing to enable customers to be more effective with their money. The FCA’s ‘access, assess, act’ framework is designed to ensure that products and services are ‘fit for purpose’. Banks need to consider the entire product lifecycle and the way that they engage with customers at each point. The end in mind becomes oriented around customers winning with their money and the bank growing through their growth. This can be measure by elements such as customers paying off their loans and then stepping up to the next money system, perhaps shifting that payment cadence to investing, demonstrating a win-win.

The provision of information at early stages of financial promotion and marketing is an obvious area of focus, as it is in the financial fitness hierarchy. As well as providing customers with content to explore at the right time of their journey as well as only providing products once they have demonstrated the right level of skills and habits to take on the demands of the product is an example of behaving with integrity towards customer success.

As regulators around the world pick up on this intent, and forward-thinking bank accelerate their shift to win-win, all banks will be forced to build business models around customer success. Given customer interactions are increasingly digital and banks will be forced to demonstrate to shareholders and regulators that they are doing everything necessary to get to customer success, the technology infrastructure requires a capability that enables customer success. Such a capability will provide the necessary controls and support that customers need to build their money systems and habits. It will in effect implement the ‘access, assess, act’ framework and then provide the ongoing support and controls around the ongoing customers actions and behaviours, guiding and supporting their success.

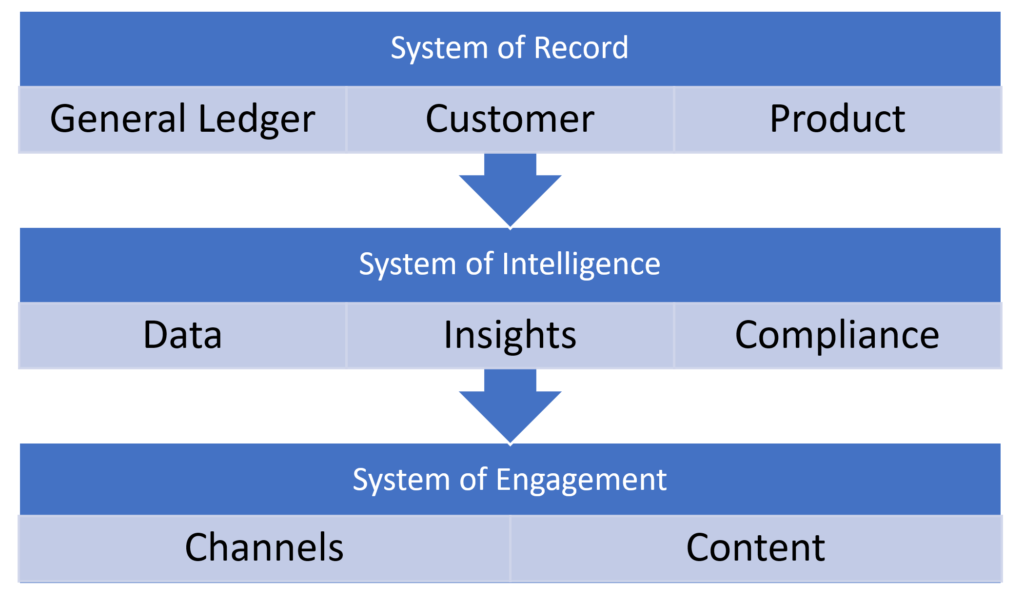

At its fullest, this capability will operate across the three primary banking systems, connecting the system or record with data and insights to drive cross channel engagement, oriented around customer success.

Moroku Odyssey as a choice

Orchestrating customer journeys using game is a powerful way to deliver win-win. There are a number of principles in game that become highly useful:

- Understand win states. Beginning with the end in mind, defining success and the plan to get there

- Establish a set of rules that define what happens when players act, rewarding them as they build skills, overcome challenges and cross through win states

- Harness game and our natural love to compete and win

As the model is deployed we begin capturing increasingly larger amounts of behavioural data, such as player archetypes, reactions to different types of reward and reward, motivations and objectives. As this data set grows our ability to then start feeding Artificial Intelligence system starts to become increasingly generative in of its own right in a customer centric fashion, something all AI is challenged with.

Moroku Odyssey is a user experience orchestration and engagement platform for financial services companies to reward and support great money habits in pursuit of engagement and loyalty. As Fintech changes the industry, customer engagement through unique experiences is a critical battleground. Moroku Odyssey and its companion design process On-Ramp and white label apps, helps banks and FinTechs provide unique and compelling experiences to attract and engage customers around a telos of wellness, architected around serious games.

Delivering personalised journeys requires a definition of what financial success means across the market, codified as a capability map that knows where customers are, where they have come from and supports their journey forward. With this in place, a rich set of intrinsic and extrinsic nudges, rewards and awards that recognise loyalty and wellness across time, space and momentum can then be triggered. Moroku Odyssey allows the customers of banks and fintechs that deploy it to unlock, understand and exercise a set of financial habits and systems that compound to achieve mastery and through that, engagement, and loyalty.

Over the last 10 years, Moroku has worked with over 100 financial service providers globally to understand and unpack money journeys. From mobile money in Africa and the underbanked in America and Bangladesh through to high-net-worth clients and some of the world’s largest banks and FinTechs in banking and payments, Moroku has built up a unique and comprehensive viewpoint that is now codified in Odyssey, a set of player maps with an initial 7 leagues, with 7 missions, 7 levels, 7 challenges and 7 archetypes to provide 16,807 initial coordinates on the map.

Players are initially positioned on the map based on their demographics and relationship history to provide the first pass and generate gratitude. This is then reflected to the customer as a set of challenges and opportunities that seem appropriate. As these are engaged with, the recommendations get better. Data can be augmented with Open Banking connectors to provide a more complete and accurate picture. Effort with other providers is also recognised, though not to the same extent as the platform provider. Odyssey accomplishes two fundamental relationship wins for banks and FinTechs:

Loyalty, recognising all the customer has done and does with their money. The money earned, saved, spent, and borrowed.

Engagement around getting into their money work across the core missions, motivating, recognising and rewarding them fort staying in the game in recognition of the age-old adage that it’s not timing the market but time in the market that builds confidence, trust and success.

We have a strong belief that this will allow banks to not only meet their customer duty obligations but also out compete the market by deploying win-win within the heart of the value proposition.