ANZ bank's proposed acquisition of Suncorp, is motivated by a need to invest more heavily in technology and to spread that burden.

During the Financial Crisis, the competition regulator, ACCC, backed the $17bn merger of St George and Westpac. 15 years on, the tides are turning with ANZ’s $5bn plan to acquire Suncorp’s banking business being rejected by the ACCC. It is a bold turnaround to drive competition, giving regional lenders, smaller banks and credit unions a leg up and encouraging them to be more ambitious.

ANZ’s ambitions with Suncorp are almost entirely technology driven. Technology is accelerating change across the world. Foreshadowed by Sci Fi writers and commentators, the robots are now here, controlling everyday outcomes from the supermarket checkout, law, war and more. Finance is fundamentally a virtual game, money an unreal story crafted to facilitate trade and therefore highly subject to digitisation. Today there is not an aspect of banking that technology cannot resolve from, from strategy and planning through product manufacture, distribution, management, and operation. It is a technology game, with the likes of AI, cloud, cyber security and mobile changing everything about banking, from how products are built, distributed, serviced and managed and it requires scale as giant tech players beat on the door.

There are enormous amounts of technology work to do, with those demands only set to increase. As this unfolds, the market will splinter in two. Large global banks with massive balance sheets with the ability to attract talent and build technology powerhouses as transaction champions, will execute strategies principled on scale. ANZ’s need and struggle with the regulator to purchase Suncorp’s banking business is an example of this playing out.

Smaller banks, unable to compete on scale, will be drawn to trusted advisor, serving niche markets with a deeper understanding and empathy of their needs. In the Australian market, Judo is perhaps a standout with its approach to SME banking. Others include Newcastle Greater who continues to build a strong community franchise in and around the Hunter Valley.

As these two trends of technologisation and separation build momentum, new patterns of manufacture and delivery are emerging. These include Bank as a Service, Composability and Personalisation. The first is the development of generic banking services, offered in the cloud, on a subscription basis to those who don’t have the economics or desire to build out generic services, wishing to focus their capital on their value-added differentiators, renting the rest in an elastic, Pay As You Go, manner. Composability is a term borrowed from the manufacturing industry and automotive in particular. VW are particularly good at it, whereby a small number of core chasses are built which are then made to look like a plethora of models and brands on demand. These come off the factory floor in line, each car different from the last. Composability creates scale and agility, key attributes in any manufacturing operation today, including finance and the ability to personalise the customer experience to the segment of one.

A New Technology Architecture

Bank as a Service and Composability require a purpose-built technology architecture. This architecture is cloud native, engineered using microservices. Rather than simply moving legacy software to the cloud, whilst retaining legacy compute models, cloud native software is engineered to fully harness capabilities, efficiencies, and scale, such as those offered by Kubernetes and a serverless paradigm.

There have been numerous attempts to shift legacy straight to the cloud. These don’t tend to go well, due to the mismatch of technology paradigms. Up until about 10 years ago, software was built in a highly monolithic way, with components highly dependent on the availability and nature of others. This severely impacts agility and their ability to operate effectively in the cloud.

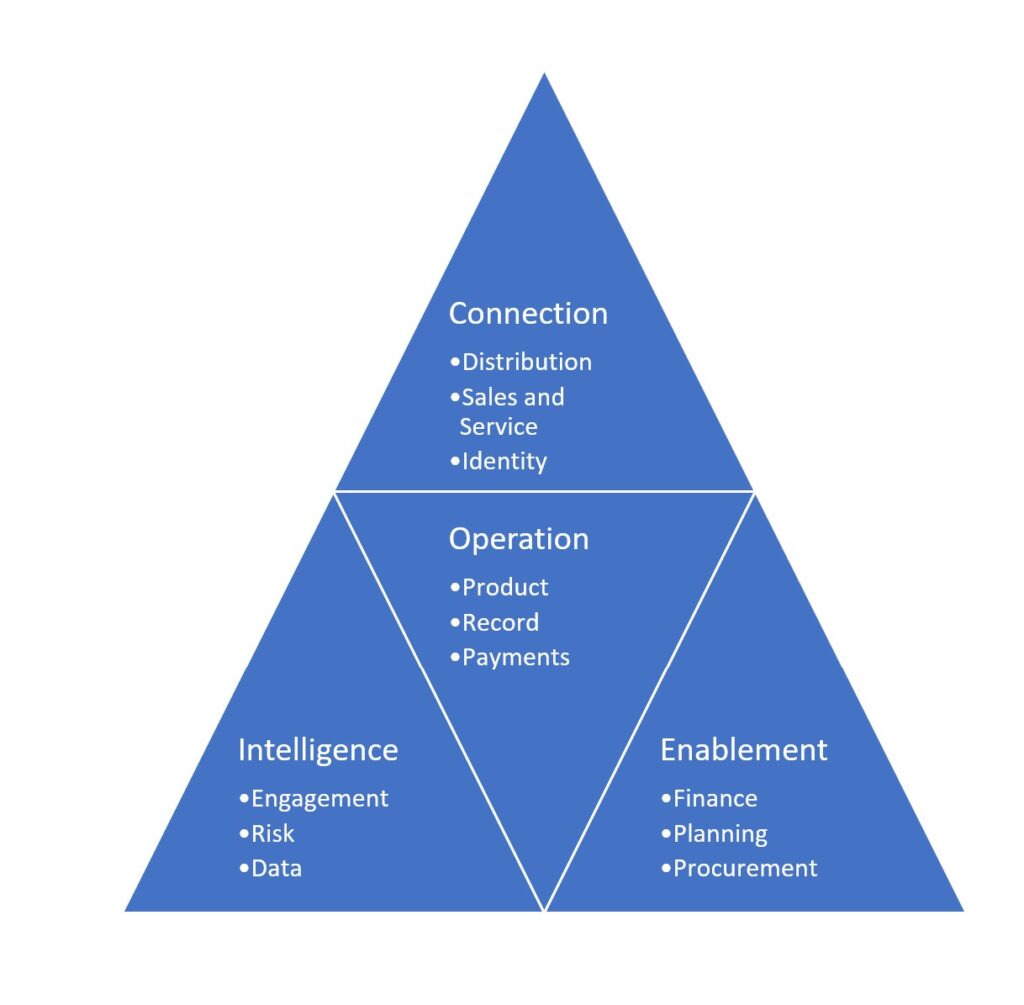

The more loosely coupled the software, the faster change can occur and the more composable the services offered. The journey to lose coupling commences by organising organisational capabilities across the four key systems of connection, intelligence, operation and enablement. With these isolated, individual components can then begin to be presented as microservices.

Moroku Money is a lightweight set of digital channels solutions as part of the system of engagement.

Moroku Odyssey provides the player maps as part of the system of intelligence. Each of these solutions is agnostics to the systems of operation and enablement.