The UK banking sector hit a wall in 2024. Profits across the industry shrank by £3.7 billion, and more than £100 billion in customer deposits quietly slipped away from high street banks to rivals offering better rates and smarter experiences. This is more than a financial shift. It is a trust migration. Customers, fatigued by sluggish innovation and impersonal service, are walking.

Behind the scenes, the big banks are grappling with rising costs: wage inflation, expensive tech upgrades, and the burden of legacy systems. Productivity is falling. Profit per employee has dropped 15%. While incumbents struggle to adapt, specialist lenders and neobanks are surging ahead, growing assets and deepening customer relationships with agility and precision. This is further evidence of a reconfiguration of the banking landscape, brought about by changing customer demands of technology & ethics.

There is a lot going on in the world, with anxiety over war, climate, the cost of living, jobs, AI, tariffs & more. Money is at the heart of how people feel & they want to be supported by the banking experience and know that their banks are behaving in a way congruent with their values.

Across America, Asia and Oceania, the conditions are strikingly similar: a concentrated banking sector dominated by a few major players, rising customer expectations, & a regulatory environment that’s opening the door to competition with Open Banking. Customers are becoming more rate-sensitive, more digitally savvy, more willing and able to switch.

Inside the banks, the pressure is building. Margins are tightening. Tech investment is no longer optional, it’s existential. And yet, many incumbents remain encumbered by legacy infrastructure and slow-moving transformation programs.

The opportunity lies with the challengers: community banks, credit unions, mutuals and neo banks with greater agility and purpose. They’re smaller, yes, but they’re also more nimble, more trusted locally, and more capable of delivering personalised, emotionally resonant experiences.

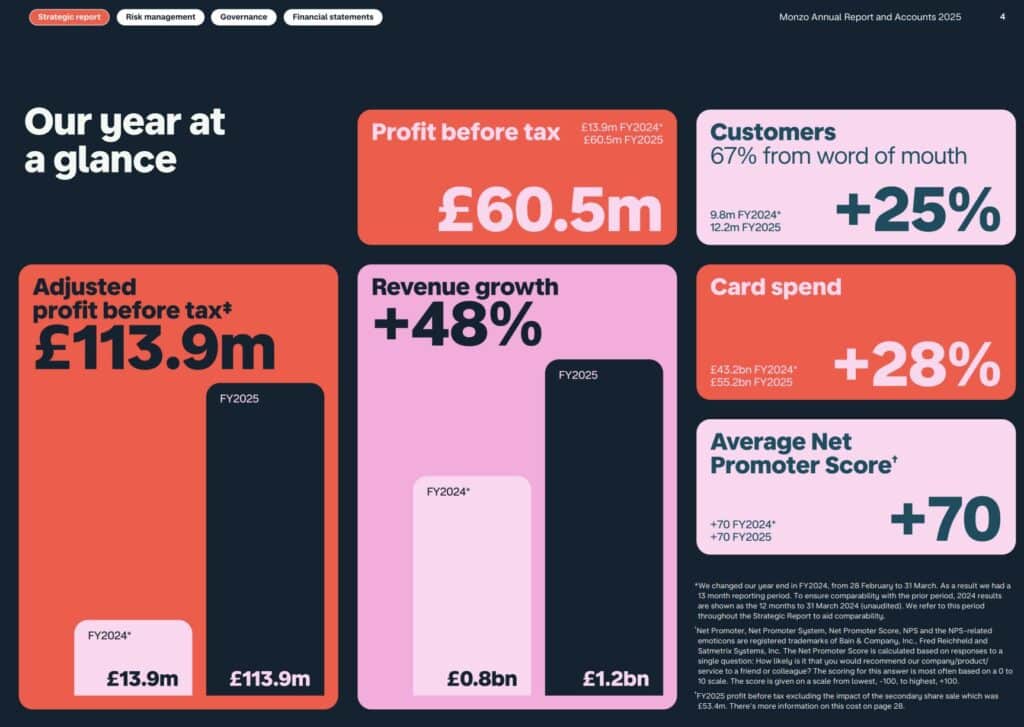

The latest figures from Monzo further reveal the seismic shift in UK banking: with over 13 million customers, including 650,000 under-16s, Monzo now serves 1 in 5 UK adults. This isn’t just growth, it’s generational entrenchment. Three cohorts are now growing up with Monzo as their first bank, embedding it into their financial identity before they even turn 18.

Traditional banks should be alarmed. Monzo added 1 million customers last quarter, with two-thirds of growth driven by word-of-mouth, a signal of deep trust and organic momentum. Its business banking arm is also reshaping norms, with 40% of customers being women, far above the UK average of 15%.

While revenue rose 48% to £1.2B, the focus remains on customer acquisition. The real test is whether Monzo can convert scale into sustainable profitability—especially without mortgages, which competitors like Revolut already offer.

But the deeper disruption isn’t just in numbers. It’s in trust. When major UK banks suffered pay-day outages in early 2025, customers missed mortgage payments and couldn’t buy food. Digital banks like Monzo stayed online. That reliability, combined with intuitive UX and emotional engagement, is redefining what customers expect from their banks.

Implications Globally

This is a preview of what’s likely to unfold globally. As younger generations seek mobile-first, emotionally intelligent banking experiences, incumbents risk losing relevance. Community banks and credit unions have a unique chance to respond—if they move fast.

With platforms like Moroku, banks can offer trust-building digital journeys that resonate with younger users, while leveraging Open Banking and composable tech to stay agile. The opportunity isn’t just to compete, it’s to redefine banking for the next generation before someone else does.

Moroku turns financial engagement into a journey, rewarding good behaviour, building muscle, and deepening trust. Our composable architecture allows banks to launch tailored solutions without the drag of legacy systems. With integrations across Open Banking, credit scoring, and document workflows, it’s built for the kind of transformation that community and challenger banks need to thrive.

In this new chapter, the winners won’t be the biggest, they’ll be the most connected, the most engaging, and the most adaptive.