The Substrate Wins: Moroku Named a 2026 ATC Semi-Finalist

Moroku has been named a semi-finalist in the 2026 Australian Technologies Competition, Growth Equity category. We’re proud of the recognition. But what matters more is what it points to.

The Institutions We Build For

Mutual banks and non-bank lenders exist to serve their communities. They were built on a different philosophy — one that puts member outcomes ahead of shareholder returns. The problem is they’ve been asked to compete in a digital world largely on terms set by the Big Four, with infrastructure priced and designed for institutions ten times their size.

That gap is what Moroku was built to close.

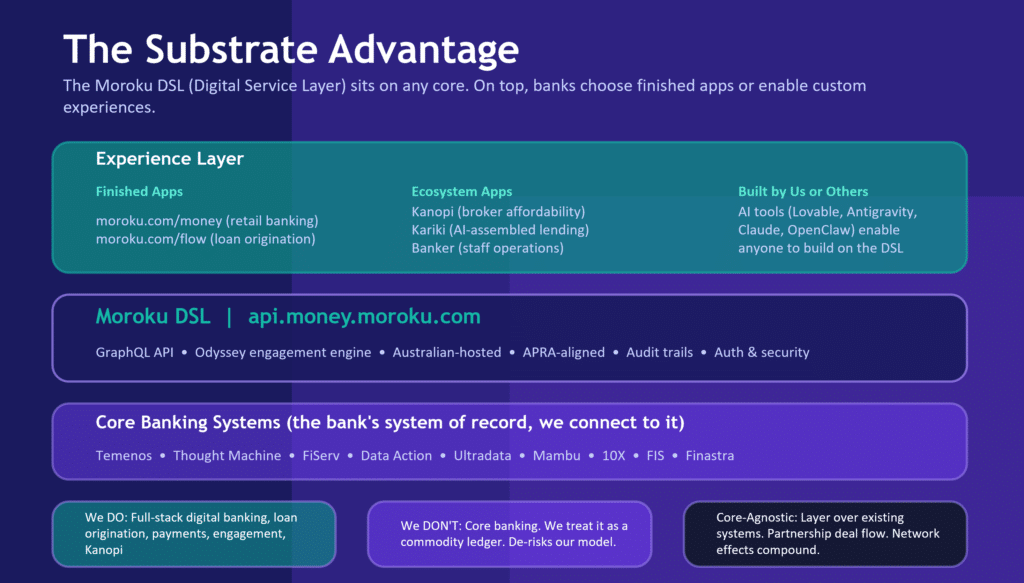

Moroku Money delivers digital banking channels purpose-built for these institutions — mobile-first, composable, and designed around a single principle: help customers win with their money. Not a portal. Not a checklist of features. A living experience that understands where a customer is on their financial journey and moves with them.

Moroku Flow handles end-to-end product and customer origination — KYC, credit decisioning, open banking integration, broker management — giving lending teams the intelligence to move fast without moving recklessly.

Together they give mutual banks and non-bank lenders what they’ve rarely had: a complete digital platform built for their scale, their economics, and their purpose.

The Layer Beneath

But the real story isn’t the applications. It’s what sits underneath them.

The industry has poured extraordinary capital into AI infrastructure — foundation models, GPU clusters, training pipelines. The assumption is that capability lives in the model. It doesn’t. The model is a tool. What the model needs to be useful is context — structured, domain-specific, behavioural context that tells it where a customer is, what they need, and what action makes sense right now.

That’s the Digital Services Layer. Moroku’s DSL assembles that context — player maps with 16,000+ coordinates, event engines, nudge libraries, psychological profiles, open banking data — into a substrate that AI agents can actually reason about. Without it, AI generates noise. With it, AI generates signal.

The models aren’t the moat. The substrate is.

Traction Beyond Our Core Market

We built the DSL for mutual banks and non-bank lenders. But the interest hasn’t stayed there.

Last week we signed another NDA with a global bank to explore use cases with our LLM priming model. Institutions at scale are running into the same problem: they have the models, they have the data, but they don’t have the structured context that makes AI produce consistent, compliant, commercially useful output. The substrate problem is universal. We built our solution from the ground up for community banking, which means it’s already embedded with the compliance guardrails, behavioural frameworks, and financial wellness logic that larger institutions are trying to retrofit.

That’s not a coincidence. It’s the architecture.

Why Now

The ATC recognition matters because of its timing. AI is repricing what’s possible in financial services faster than most institutions can respond. The cost barriers that kept challengers out — technology, compliance infrastructure, decisioning capability — are collapsing. The window for mutual banks and non-bank lenders to move is open. It won’t stay open indefinitely.

Recognition like this doesn’t close deals. But it confirms that what we’re building is real, that the timing is right, and that the market is starting to see what we see.

The substrate wins.