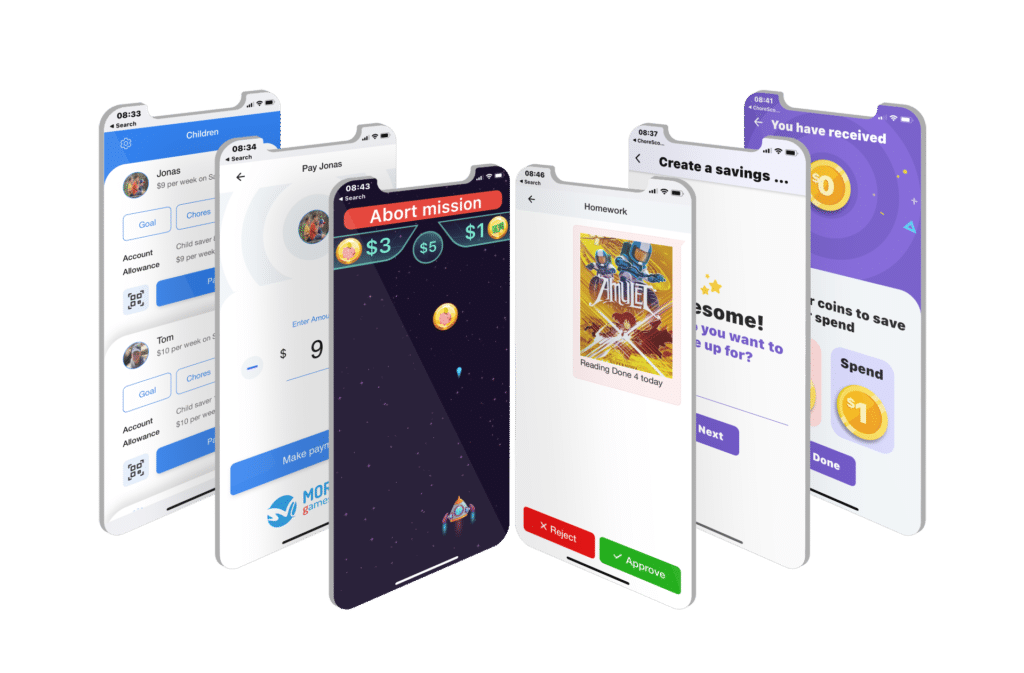

Banking Children and Their Families

Chore Scout is a white label children banking for banks and credit unions that want to bank the next generation of customers and their families on a foundation of strong money habits.

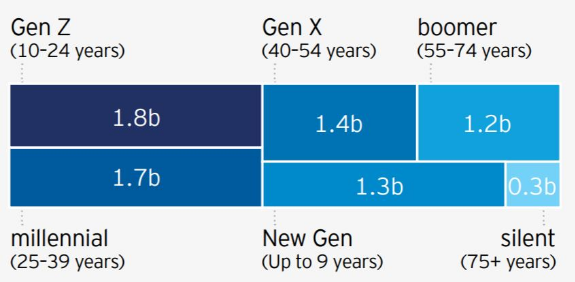

GENERATION Z - THE LARGEST COHORT IN THE HISTORY OF THE PLANET

While millennials today are having their moment, the next decade will be shaped by the maturation of the largest generational cohort in history — Generation Z. This cohort of people between 10 and 24 years old comprises 1.8 billion people, making up 24% of the global population.

As the EY Megatrends report informs us, while Gen Z is generally more progressive on social issues than preceding generations, important differences in attitudes emerge. Gen Z is socially conservative and feels more pressured to succeed. Brands will do well to identify the important distinctions among Gen Zers to serve this global cohort effectively and begin building that intelligence and rapport now.

The next decade will be shaped by the maturation of GENERATION Z, the largest generational cohort in history

The Business Case

ChoreScout Case Study

Financial Fitness for Families is Paramount

Parents are the gateway. 87% of high school student acknowledge that they consider their parents as a primary resource to seek financial information but only 22% reported to talk frequently to their parents about money. Banks can step in, facilitate the conversation, build trust and market share.

Few financial institutions focus on children as this market segment has been perceived for a long time as difficult and challenging. Yet those that pioneer in providing financial fitness through digital to children enjoy a wide range of benefits from creating a socially responsible reputation to greatly increasing their customer base before competitors realize the opportunity. Children have more chances to become financially literate adults if they are exposed to appropriate financial education programs and activities from their childhood. This is supported by general sociology that indicates that our beliefs are baked by early teens if not before. Friedline and Elliott (2013) concluded that young adults who had a savings account as a child are two times more likely to have a savings account in their adulthood.